Newsletter

A weekly data digest for the leading crypto investors and operators.

Token Terminal Research

•

Introduction

This week’s newsletter covers the Lending market sector. We zoom out and reflect on how the sector has evolved over the past three years, and highlight a few emerging projects that have grown their market share meaningfully over the past few quarters.

Let’s jump in!

- The historical borrowing volume reflects the varying nature of leverage within the DeFi market, with periods of increased borrowing corresponding with bullish market sentiment, and vice versa

- The initial growth phase coincided with the launch of the COMP liquidity mining campaign in June 2020. The correlation underscores the impact that token incentive programs can have on market adoption and growth. However, the chart also highlights the sustainability challenges of such programs, as evidenced by the subsequent contraction from the peak in 2021.

- Outstanding borrows peaked at $23 billion in December 2021, and bottomed at $3.6 billion in January 2023. The subsequent recovery to $8.3 billion illustrates the market's resilience and potential for future growth.

- The integration of real-world assets (RWAs) as collateral, in addition to crypto-native assets, represents a significant opportunity for market expansion.

- Contrary to the notion that open-source crypto protocols lack moats, the data indicates that certain protocols, such as Aave, have established significant market dominance. Aave has maintained ~50% market share for three consecutive years, while Compound, another leading DeFi lending protocol, has experienced a decline in its market position over the same period.

Growth strategies in the lending market sector:

- “Vampire attack”: Morpho built an aggregator on top of Aave and Compound, to rapidly capture both mind and wallet share in the market, while simultaneously building a new separate protocol of their own called Morpho Blue.

- “Partnership”: Spark taps into the established brand and liquidity of Maker by operating a lending protocol as a subDAO within the broader Maker system.

- “Blue ocean”: Venus has decided to double down on the BNB Chain ecosystem, where many of the “Ethereum-first” lending protocols have yet to establish a strong presence.

- The lending market, similar to traditional financial markets, is governed by power laws, where a small number of players control a large portion of the market.

- The entry of new competitors increases competition and innovation, which are likely to lead to faster development of superior products. This heightened competition benefits both application developers building on top of lending protocols, and consumers that interact with these applications.

- Benqi's rapid growth in 2021 exemplifies the volatile nature of the DeFi lending market. Despite its initial surge, Benqi (in light purple above) has subsequently shrunk to a smaller role within the market. Further, all projects in the market face risks related to early-stage technology, something that was exemplified by the oracle bug on Euler (in brown above), which resulted in a significant drop in use overnight.

- A notable development during Q1 was that both Spark and Morpho surpassed Compound in terms of outstanding loans.

- Daily active users (DAUs) are calculated based on user actions such as deposits, borrows, repayments, and withdrawals. The DAU metric does not account for users who passively earn interest or have their assets lent out. One should keep this in mind when analyzing the DAU figures above.

- A significant portion of the lending protocol user base may comprise aggregators, such as wallets or other protocols, rather than individual users. This can result in high monetary values, even with low DAU counts.

- Venus tends to experience rapid spikes in active loans during BNB Launchpool listings. This suggests that users seek leverage to farm new tokens.

- Morpho's approach to user incentivization, involving a non-transferable governance token (MORPHO), allows for user rewards without immediately creating a liquid market for the token. This in contrast to immediately liquid token incentive models, such as Compound's, which tend to attract short-term, opportunistic capital.

Definitions:

- Net deposits: user deposits aka money coming into the protocol.

- Active loans: user deposits loaned out to borrowers.

- Total value locked (TVL): difference between net deposits and active loans, TVL represents the amount of capital that is currently held within the protocol but not loaned out to borrowers.

- Implications of (high/low) TVL: a high TVL suggests that a considerable portion of the capital within the protocol remains idle. For instance, Aave’s $7 billion in TVL indicates that a large amount of user deposits are not actively loaned out (to generate revenue for the Aave DAO).

Capital efficiency versus prudent risk management:

- Aave's substantial TVL (Net deposits - Active loans) may reflect a more conservative risk management strategy, ensuring that capital is available within the protocol to meet withdrawal demands and mitigate risks.

- Morpho's relatively low TVL (Net deposits - Active loans) indicates an approach that leans towards capital efficiency. This approach maximizes the utilization of deposited funds, but may entail higher risk if not managed carefully.

- For deeper operational and risk-related insights, one should review the collateral asset breakdowns, collateral ratios, and interest rate mechanisms.

- Morpho started with a lending aggregator product, built on top of Aave and Compound, and after reaching ~$1B in deposits, introduced a new separate product called Morpho Blue.

- Morpho Blue adopts many of the best practices introduced by Uniswap: permissionless market creation, immutable smart contracts, and a minimalistic code base → a secure and scalable protocol.

- For readers, it’s worth keeping an eye on the growth of Morpho Blue, as it could grow into one of the most widely used lending protocols in DeFi.

The Token Terminal Data Partnership

Are you in charge of 📊Data analytics or 📈Growth/BD at an L1, L2, or appchain's Foundation/Labs?

— Token Terminal 📊 (@tokenterminal) January 26, 2024

Regardless of the stage the chain, the Token Terminal Data Partnership™ is a turnkey solution that ensures the availability of a

1) reliable & scalable Data Pipeline,

2)… pic.twitter.com/2DEYlCFOOY

We're thrilled to partner with @Calderaxyz, the market-leading RaaS platform, to make institutional-grade onchain analytics & standardized reporting available to Caldera Chains!

— Token Terminal 📊 (@tokenterminal) February 9, 2024

Interested? Read on!

Are you in charge of 📊Data analytics or 📈Growth/BD at the Foundation/Labs of… pic.twitter.com/ZTelsIPiu9

Our mission is to provide technology services to the 8 billion people across the globe. 🌐🚀 https://t.co/mr173re5LQ

— TRON DAO (@trondao) February 7, 2024

Learn more: https://tokenterminal.com/data-partnership

📣 Insights from our community

Data-driven insights from analysts using Token Terminal PRO

This chart from @tokenterminal comparing friendtech's revenue with tvl is pretty telling.

— Joel John (@joeljohn) February 8, 2024

In the absence of points (or tokens), revenue on the platform declined 90% (from $1mil/day to ±$15k) but TVL has declined only about 50% (±$50m to $26mil).

Makes me think users bridged… pic.twitter.com/cMu68Kq6CE

How to spot trends and go deeper using onchain data:

— Michael Nadeau | The DeFi Report (@JustDeauIt) February 11, 2024

1. Start with high-level comparison data: we look at the top blockchains and do relative comparisons across users, revenues, transactions, TVL, DeFi metrics, number of projects etc.

2. Look for trends. In the video, we saw… pic.twitter.com/t1GJzi71hz

We're early in the game, but it's clear: Investing in coins & tokens with economic traction outperforms across the crypto cycle. It boosts investor confidence in protocols with real usage. Our dynamic index strategy ensures we don't hold onto the last cycle's losers.… https://t.co/RAJ9ZuPp8n

— Martin Leinweber (@mleinweber2) February 12, 2024

ICYMI

Explore the Terminal: https://tokenterminal.com/terminal

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

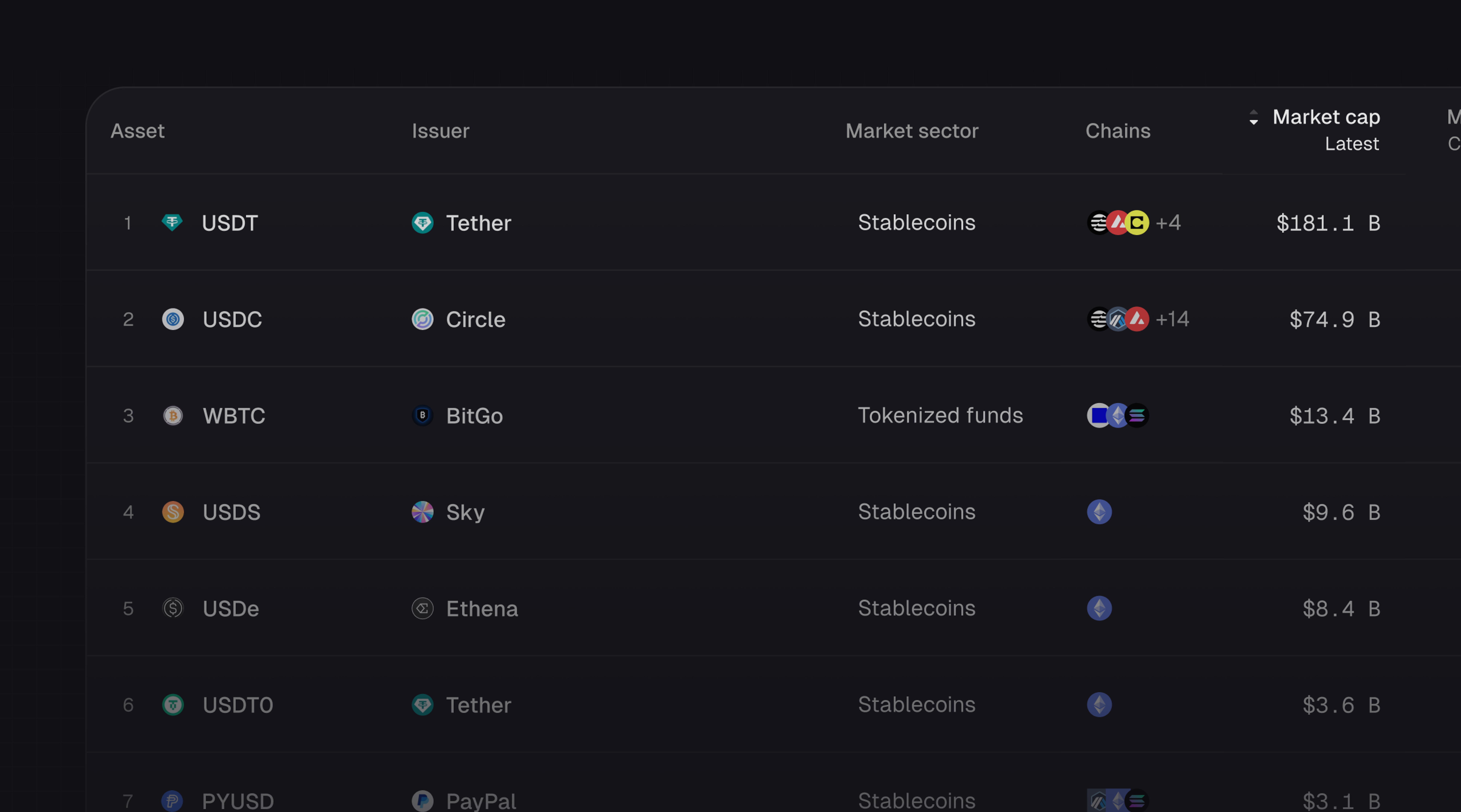

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.