Newsletter

Crypto fundamentals – Charts and trends to watch

Token Terminal

•

A walkthrough of the most interesting charts and trends in crypto, with a focus on key business drivers and protocol fundamentals.

This week’s newsletter focuses on the stablecoin issuers market sector, which has a designated dashboard on Token Terminal. Let’s dig in!

Decentralized stablecoin issuers are smart contract-based credit facilities that allow users to borrow stablecoins (often pegged to the dollar or euro) against crypto or real-world collateral assets.

Introduction

- Stablecoin issuers allow users to borrow stablecoins against crypto or real-world collateral assets. Stablecoins are typically pegged to the value of real-world fiat currencies, such as the US dollar or the Euro. Once a user has deposited collateral into a stablecoin protocol, they’re able to borrow stablecoins minted by the protocol. Compared to lending protocols, where other users are the source of funds for borrowers, here the stablecoin issuer is the counterparty.

- Stablecoins provide an alternative store-of-value to volatile onchain assets. The value of native onchain assets such as BTC and ETH tends to fluctuate wildly. Users who wished to keep their assets onchain were subject to this volatility. As a result, stablecoins were developed as a means to allow users to store and transfer their onchain value without fear of price instability.

- Most stablecoins can only be minted with overcollateralized user deposits. While overcollateralized stablecoins are less capital efficient, they allow for a more robust peg. On the other hand, algorithmic stablecoins (such as Terra’s UST) achieve price stability through algorithms that control their circulating supply and do not require excess collateral. However, most (if not all) algorithmic stablecoins to date have failed over the long term, due to users exiting their position rapidly once prices fall below peg.

Overview

The daily outstanding supply of the top 18 projects in the stablecoin issuers market sector since the beginning of the year is visualized below.

Scope of analysis

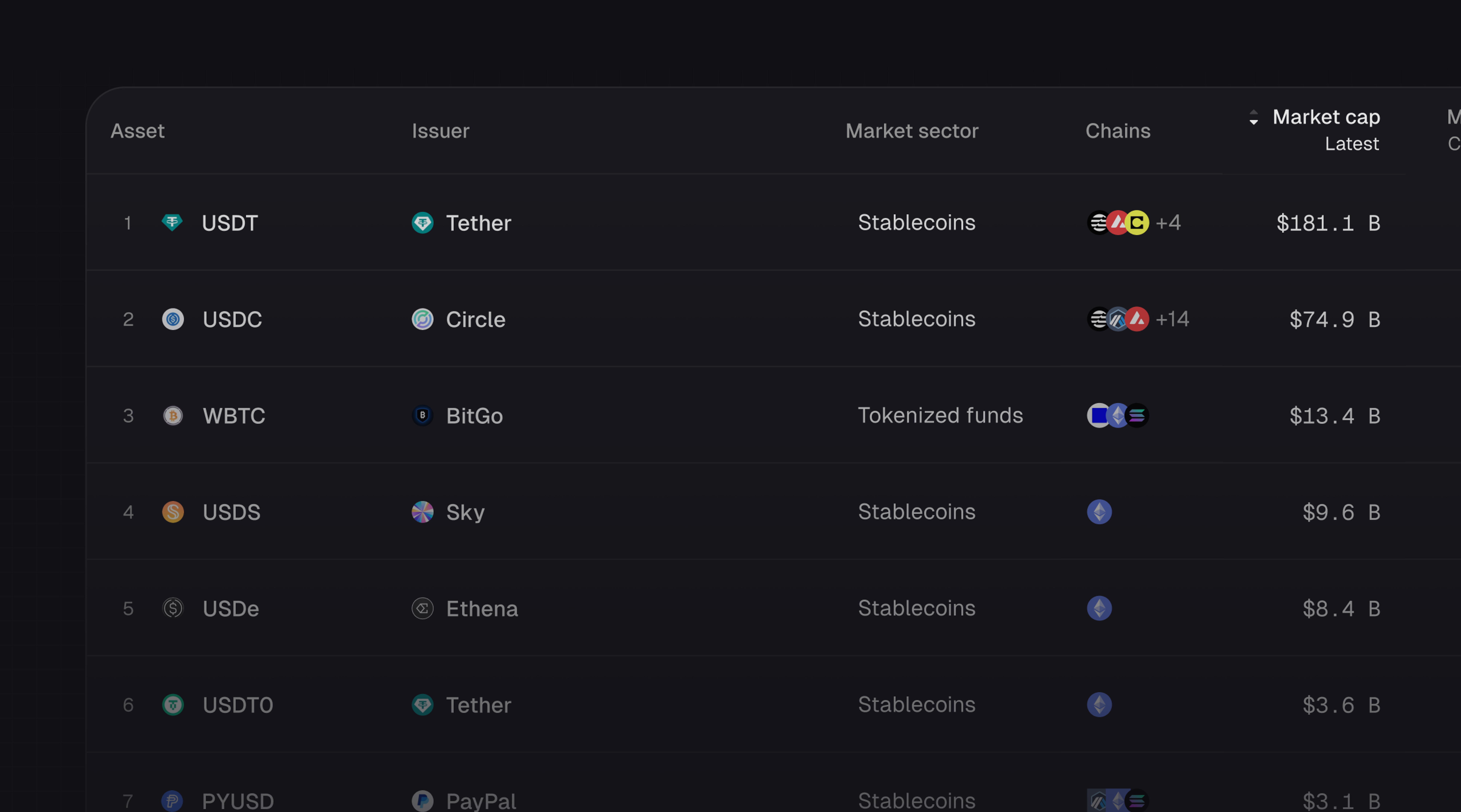

- The stablecoin issuers dashboard features 18 projects. There are numerous stablecoin issuers not yet listed on Token Terminal, so the dashboard can only give an indicative analysis of the market sector.

- Outstanding stablecoin supply has been trending down year-to-date (YTD). Since January 1st, the outstanding supply of stablecoins has decreased from $100b to just $76b.

- Circle (USDC) and Paxos (BUSD) experienced the largest drop in outstanding supply. Although USDC was the largest stablecoin by outstanding supply at the beginning of the year, its outstanding supply has since dropped from $42.2b to $25.1b (-40.5%). Similarly, BUSD outstanding supply decreased from $17.4b to $3.9b (-77.6%) over the same time period.

- This decline was largely driven by macroeconomic and regulatory factors. In March, Circle announced they had up to $3.3b in exposure to the struggling Silicon Valley Bank. As a result, the price of USDC fell under $1, and the outstanding supply has been on a continuous decline since. Similarly, the New York Department of Financial Services (NYDFS) instructed Paxos to cease minting BUSD in February. The outstanding supply of BUSD decreased from $15.0b to $9.1b over the following month.

- Despite this, centralized fiat-backed stablecoins still dominate the stablecoin market. Centralized stablecoins currently represent over 90% of the total outstanding supply. MakerDAO’s DAI, the largest decentralized stablecoin by outstanding supply, only makes up ~6% of the current total market share.

MakerDAO: liquid-staking tokens gaining popularity as collateral

- Deposits in MakerDAO’s wstETH (WSTETH-A and WSTETH-B) vaults have grown from $657m to $2b (+200%) YTD. wstETH is the wrapped version of Lido’s Ethereum liquid staking derivative (LSD). At the beginning of the year, wstETH represented less than 12% of MakerDAO’s total collateral. As of August 17th, this share has risen to over 40%. Read more on liquid staking in a previous edition of our newsletter here.

- Yield-bearing forms of ETH have been gaining popularity since Ethereum’s Shapella upgrade. Following Ethereum’s Shapella upgrade in April, ETH stakers were allowed to withdraw their staked assets from the beacon chain. This drastically reduced the risks associated with LSDs. This encouraged more users and protocols alike to use and support LSDs, as this is a yield-bearing form of ETH.

- We anticipate more stablecoin issuers to build products around LSDs. Large existing stablecoin issuers such as MakerDAO are beginning to support LSDs as collateral. In addition, emerging stablecoin issuer protocols such as Lybra Finance and Raft are launching with LSDs as their sole collateral.

- We also expect this trend to extend to staked versions of other native blockchain assets, such as MATIC and SOL. An example is Davos Protocol, a new stablecoin issuer on Polygon that supports staked ankrMATIC as collateral. As the proportion of staked assets on Polygon and Solana are much higher than on Ethereum (70% vs 20%, respectively), the potential for LSDs to act as collateral is also greater on a relative scale.

Liquity: Outstanding supply of LUSD has increased by 25% since the USDC depeg in March

- LUSD’s outstanding supply has grown from $233m to $293m (+25%) since the USDC depeg in March. Liquity supports the minting of their stablecoin LUSD with ETH as the sole collateral. Over this same period, the value of ETH collateral deposits (total value locked) has also increased from $551m to $907.8m (+65%).

- Demand for stablecoins with uncensorable collateral is rising due to mounting macroeconomic and regulatory risks. As mentioned above, unstable macroeconomic and opaque regulatory factors have prompted users to prefer collateral that cannot be easily mismanaged or seized. This trend reflects a broader movement within the cryptocurrency industry toward decentralization and resistance to external control.

- Different collateral types represent tradeoffs for stablecoin issuers. Fiat collateral allows projects to scale their outstanding supply more effectively but is generally subject to higher management and centralization risk as collateral needs to be stored offchain. On the other hand, uncensorable and fully onchain collateral such as ETH is less capitally efficient but offers non-custodial management of user deposits. Decentralized stablecoin issuers need to take these factors in mind when deciding which collateral types to support.

Aave GHO: GHO’s outstanding supply reached $21.8m within a month of launching

- Leading lending protocol Aave’s stablecoin GHO has reached ~$21.8m outstanding supply within a month of launch. Aave uses a unique model, where GHO can be minted with user collateral deposited in Aave’s lending pools. Users are able to simultaneously earn yield on their supplied collateral while paying interest on their GHO position.

- To support the growth of GHO, Aave is offering minting discounts to AAVE stakers. AAVE token holders who stake their governance tokens in the Aave Safety Module are offered a discount when minting GHO. When borrowers contribute to the Safety Module, they are accepting the risk that their staked amount may be used to cover any deficit that arises from bad debt.

- GHO represents a new revenue source for the Aave DAO. All interest payments accrued by minters of GHO go directly to the Aave DAO treasury. As Aave’s governance extends to GHO, this also introduces an additional utility to the AAVE token.

- Aave has over $4.8b in total value locked (TVL), so there remains significant potential for the growth of GHO. The current outstanding supply of GHO remains a small fraction of total Aave’s TVL. This indicates that the majority of users who have deposited assets in Aave have yet to mint GHO. The untapped potential of GHO, along with the synergies it has with the rest of the Aave ecosystem, make it a critical element for the future growth of the protocol.

Other key highlights from the stablecoin issuers market sector

Circle

- On August 10th, Bloomberg published an exclusive article detailing Circle’s recent financial performance. The article highlights that Circle generated over $779m in revenue in the first half of 2023 alone. As of June 2023, the company has over $1b on its balance sheet.

Liquity

- On July 28th, Liquity introduced v2 of their protocol. This new version introduces two key features - principal protection, and subsidized secondary markets.

- Principal protection offers users a mechanism to protect their positions from losses during market downturns, making the hedging position more attractive for users even under difficult market situations.

- Subsidized secondary markets allow users to trade their hedging positions at greater price efficiency, which mitigates risk in the case of volatile asset prices.

MakerDAO

- On August 7th, MakerDAO activated the Enhanced DAI Savings Rate (EDSR), allowing DAI depositors to earn up to 8% in yield (up from the previous 3.3%). Since EDSR was introduced, MakerDAO’s TVL has increased by more than $700m.

Membrance Finance

- On May 29th, Membrane Finance launched the EUROe Account API, which enables programmatic minting, burning, and bridging of EUROe across all supported blockchains.

- In addition, the protocol has announced multiple partnerships over the past months. Prominent examples include integration with fiat-crypto gateway service Mt Peterin allowing for on/off-ramps with zero fees, and a low-slippage OTC trading integration for EUROe with trading desk Woorton.

Origin Protocol

- Origin Protocol’s OUSD was the first yield-bearing stablecoin in DeFi, earning yield through major DeFi protocols such as Curve, Aave, and Compound. Origin Dollar plans to integrate with Flux Finance and MakerDAO’s DAI Savings Rate. With the addition of these strategies, users can benefit from competitive yields on DAI, as well as gain a proxy to yield from US treasury bonds.

PayPal (Paxos)

- On August 7th, PayPal unveiled PYUSD, a stablecoin pegged to the US dollar backed by dollar deposits, US treasuries, and cash equivalents. The stablecoin will be issued by Paxos, the previous issuer of BUSD. PYUSD is to be launched on Ethereum, and can be used for payments on the PayPal website.

Changelog

Recent updates and improvements to the stablecoin issuers market sector on Token Terminal.

| Action | Business impact |

|---|---|

| New listing of Aave GHO. | New listing of GHO stablecoin. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| New listing of FRAX stablecoin. | New listing of FRAX stablecoin. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| New listing of Inverse Finance. | New listing of DOLA stablecoin. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| New listing of Paxos. | New listing of Paxos. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| New listing of Gemini. | New listing of Gemini. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| New listing of Archblock. | New listing of Archblock. This has increased Token Terminal’s coverage of the stablecoin market sector. |

| Add Arbitrum support for Circle. | Allows Token Terminal to provide more accurate and up-to-date data for Circle. |

Video of the week

In this episode of the Fundamentals podcast, we’re joined by Evan Fisher, the founder of Portal Ventures – a fund that is accelerating the protocol economy through business fundamentals.

Portal Ventures identifies and supports crypto businesses that will define the next generation of our economy. They advise on strategy, roadmap, go-to-market, value capture, fundraising, and more.

Listen to the episode

In this episode with Evan, we discuss Portal Venture, their investment strategy, and how they work with the projects they invest in. We cover what makes crypto interesting, and what the most common misconceptions are that traditional investors have about the asset class.

We also break down the pros and cons of liquid venture, discuss crypto business models, and speak about whether crypto projects are software or marketplace businesses. Finally, Evan shared what he is most excited about in crypto right now. Tune in for a great discussion about the fundamentals of the protocol economy.

Timestamps:

00:00 Introduction

00:58 Evan’s introduction & background

02:53 Overview of Portal Ventures

05:12 The problem that Portal Ventures solves for investors

07:40 Is Ethereum a marketplace or a software business?

10:10 The biggest misconceptions that traditional investors have about crypto

13:28 Crypto business models & how does Evan approach valuing early-stage projects that don’t yet have cashflows?

15:27 The pros and cons of liquid venture

18:24 Portal Ventures’ investment underwriting process: sourcing, diligence, decision-making

22:06 What stage does Portal Ventures invest at?

23:25 Does every investment need to be able to theoretically return the fund?

25:30 How does Portal Ventures utilize data?

27:41 How does Portal Ventures work with the projects they invest in?

31:22 A need for more non-technologists in crypto

32:03 Investment case: Blueprint (Concrete)

35:10 What is Evan most excited about in crypto right now?

37:30 The biggest challenge that funds face in this space today

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.