Newsletter

Crypto fundamentals – Charts and trends to watch

Token Terminal

•

A walkthrough of the most interesting charts and trends in crypto, with a focus on key business drivers and protocol fundamentals.

This week’s newsletter focuses on the liquid staking market sector, which has a designated dashboard on Token Terminal. Let’s dig in!

Liquid staking projects allow users to stake their assets and maintain liquidity via a derivative liquidity token (liquid staking derivative, LSD) that represents the underlying asset.

Introduction

- Liquid staking projects allow users to stake their assets and maintain liquidity via a derivative liquidity token (liquid staking derivative, LSD) that represents the underlying asset. Proof of Stake (PoS) blockchains reward users that stake their assets with staking rewards, as these users contribute to block validation and greater network security. Liquid staking projects typically generate revenue by taking a cut of the staking rewards generated.

- Liquid staking projects reduce the opportunity cost of locking up capital when participating in staking. As staking in PoS blockchains require users to lock up their funds, this presents an opportunity cost to the user. However, liquid staking projects unlock that liquidity by allowing users to access LSDs.

- As PoS blockchains rise in popularity, so does the demand for liquid staking projects. Most widely-used blockchains (L1), including Ethereum, now run on PoS. As a result, liquid staking projects have tremendous potential for growth, as they are able to unlock the liquidity of the staked native tokens of these blockchains.

- The number of projects building on top of liquid staking projects is also increasing. Prominent DeFi projects such as MakerDAO and Aave now allow users to deposit wstETH, the wrapped version of Lido’s Ethereum LSD, as collateral. Emerging projects such as Raft are also building their R stablecoin using LSD tokens as collateral.

Overview

The daily assets staked of top projects in the liquid staking marketplace sector since the beginning of the year are visualized below.

Scope of analysis

The liquid staking dashboard features 15 projects, and covers the majority of the liquid staking projects currently live.

- Assets staked across liquid staking projects have seen a rapid increase since the beginning of the year. Aggregated assets staked have grown from approximately $7.8b in January to an all-time high of over $20b today, an increase of 156%.

- Key drivers behind this growth were an increase in ETH price and Ethereum’s successful Shapella upgrade. The price of ETH rose from ~$1200 at the beginning of the year to ~$1850, as of August 1st. In addition, Ethereum’s Shapella upgrade in April enabled the withdrawals of staked ETH from the Beacon Chain back to Ethereum’s execution layer. This significantly reduced the risk related to ETH staking, resulting in more users willing to stake their assets.

- Lido remains the market leader in the liquid staking sector, with a 75% market share of assets staked. Lido was the first liquid staking project to launch, releasing their product in December 2020. As the success of liquid staking projects is heavily dependent on the adoption and liquidity of their derivative tokens, Lido’s first mover advantage has allowed them to capture the majority of liquid staking market share.

- The liquid staking market sector still has room to grow. Only ~20% of the total ETH supply has been staked, which still is relatively low compared to other PoS chains. Examples include Solana and Avalanche, both of which currently have staking ratios of over 60%. Given the higher market capitalization of ETH (~$222b as of August 2nd, 2023), we could potentially see multibillion-dollar growth in assets staked over the coming quarters.

Centralized staking providers tend to charge higher commissions on ETH staking

- The fees charged on ETH staking rewards generated range from 10% to 25%. The primary business model of liquid staking projects is to charge a commission on the ETH staking rewards generated. The median commission charged on the rewards generated is 10%. The commission either goes directly to the project or in some cases is split with external node operators running the validators.

- Centralized exchanges are able to charge a higher commission compared to their onchain counterparts. Centralized exchanges offer a relatively seamless staking experience, and are able to attract new users unfamiliar with onchain projects. As they allow new users to access staking yields that they otherwise would not be able to, exchanges also tend to charge higher staking commissions.

- Increased competition has yet to drive fees lower. Although the number of liquid staking providers has increased, this has yet to result in lower commissions, with fees staying relatively flat. In particular, the majority of onchain ETH staking providers still charge 10% on staking rewards.

Liquid staking providers and their number of node operators

- Major liquid staking providers on Ethereum have used different go-to-market strategies. Rocket Pool and Stader allow anyone to become a node operator, which enables existing node operators to earn additional yield while also decentralizing the project. All other liquid staking providers currently rely on hand-picked external node operators and/or operate their nodes themselves.

- Permissioned or private node operators are easier to operate and manage. Collateral, technical, and security-related risks make it more complex to run on a permissionless node operator set. To shorten their launch time, many liquid staking providers have decided to initially rely on permissioned or private node operators.

- There is an increasing demand from consumers for more decentralized and permissionless liquid staking service providers. Ethereum operates with an ethos of decentralization, which encourages as many different node operators as possible to maintain network security. As major projects such as Lido currently still use a smaller number of permissioned node operators, some Ethereum users have expressed concerns over the centralizing effect this would have, should Lido continue to gain more market share. Numerous projects are working on a more decentralized staking model, with prominent examples including StakeWise v3 and Lido v2.

Other key highlights from the liquid staking market sector

Lido

- Lido v2 officially launched on Ethereum mainnet on May 15th. As a result of this upgrade, users are able to exit their stETH position to ETH at a 1:1 ratio. Even after withdrawals were enabled, the total assets staked via Lido have continued to rise.

Stader

- On July 10th, Stader launched ETHx, their liquid staking token on Ethereum. Since then, over 8000 ETH ($15M+) has been staked with Stader on Ethereum. In addition, Stader also has liquid staking products on other chains, including BNB Chain and Fantom.

StakeWise

- On July 17th, StakeWise announced the deployment of StakeWise v3 on Ethereum testnet. Jordan Sutcliffe, Business Development Lead at StakeWise, also held a presentation introducing the project during ETHCC.

Swell

- Swell recently introduced a link to DEX aggregator ParaSwap on their staking interface, where users can purchase swETH on the secondary market with a lower price impact. To date, over 10k users have now staked ETH for swETH on Swell, with the value of assets staked above $80m.

Rocket Pool

- Rocket Pool’s Atlas upgrade went live on April 18th. Following the upgrade, users could become a node operator by providing just 8 ETH, instead of the previous requirement of 16 ETH. This significantly increases the capital efficiency and profitability of Rocket Pool node operators. Since the upgrade, the assets staked using Rocket Pool have grown from around $1b to over $1.6b.

Changelog

Recent updates and improvements to the liquid staking market sector on Token Terminal.

| Action | Business impact |

|---|---|

| New listing of Jito. | New listing of a liquid staking project on Solana. This has increased Token Terminal’s coverage of the liquid staking market sector. |

| New listing of Marinade. | New listing of a liquid staking project on Solana. This has increased Token Terminal’s coverage of the liquid staking market sector. |

| New listing of Stader. | New listing of a liquid staking project on Ethereum & other blockchain. This has increased Token Terminal’s coverage of the liquid staking market sector. |

| New listing of Swell. | New listing of a liquid staking project on Ethereum. This has increased Token Terminal’s coverage of the liquid staking market sector. |

| Addition of Lido’s stMATIC assets staked. | Addition of Lido’s stMATIC business line. This has increased the depth of the Lido dashboard on Token Terminal. |

Video of the week

In this episode of the Fundamentals podcast, we’re joined by Getty Hill, the Co-Founder of GFX Labs, a multi-faceted blockchain research and development company. GFX Labs operates as both a crypto products studio and an active DAO governance contributor.

Listen to the episode

We speak about how GFX operates, the current state of DAO governance, and what an ideal DAO could look like. We dive into Uniswap’s fee switch and GFX’s stance on it, and also discuss the onchain borrow-lend market sector, the biggest opportunities and challenges in that space, and much more!

Timestamps:

00:00 Introduction

01:06 UniswapX: first impression

03:38 Overview of GFX Labs

04:50 The core problem that GFX Labs solves

06:25 How does GFX Labs fund operations?

10:00 A primer on DAO governance

11:12 Which DAOs stand out as of today?

12:43 How does GFX Labs approach and contribute to DAO governance?

14:15 Current voting power

16:12 Is DAO governance professional enough yet?

19:10 The shortcomings in current DAO governance models

22:12 Is voting power too centralized?

23:17 The Community Proposal Factory (CAP): what and why?

24:48 The problem with Snapshot voting

25:54 The amount of effort that goes into governance proposals

28:23 Uniswap's fee switch

31:02 Why is now the right time to turn on the fee switch?

34:54 Where have previous fee switch proposals fallen short?

36:40 State of the onchain lending market

38:40 Undercollateralized lending in DeFi

41:12 Current opportunities within the lending market sector

42:10 What's next for GFX Labs? Oku Trade

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

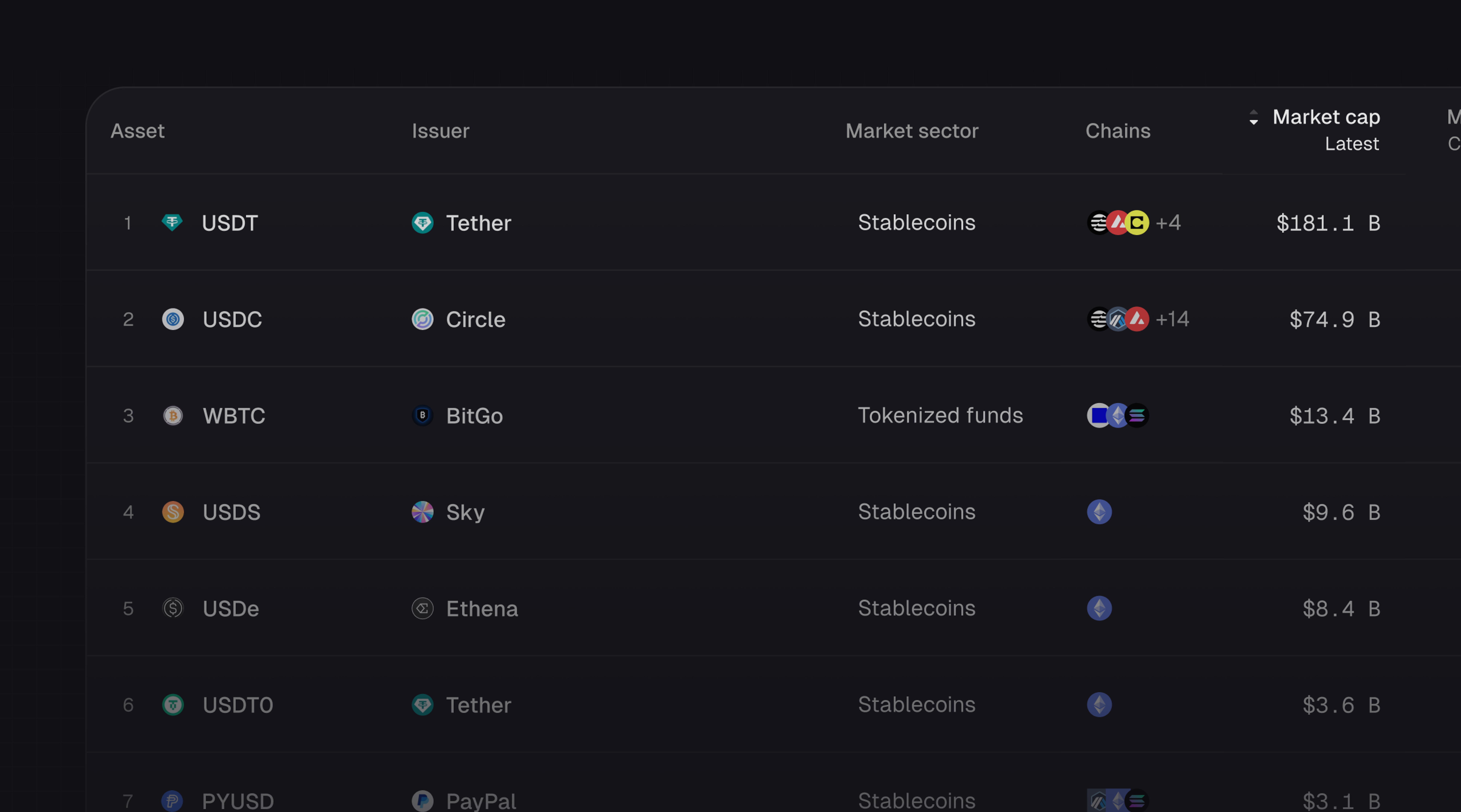

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.