Newsletter

Weekly fundamentals – Exploring the liquid (re)staking market sector

Token Terminal Research

•

📊 New listings

Holdstation DeFutures – a non-custodial perpetual exchange protocol built on zkSync Era.

Holdstation DeFutures offers traders the opportunity to trade multiple assets with leverage up to 500x. Liquidity providers deposit funds into DeFuture Vaults and receive trading fees from traders (supply-side fees). Holdstation currently takes a cut of the total trading fees paid by traders (revenue).

- The trading volume on DeFutures has grown rapidly since November '23, reaching a cumulative $1.8B over the past 180 days.

- Over the same period, the monthly average revenue per user (ARPU) has increased by 227% from $4.9 to $16.0, with monthly active users (MAU) currently sitting at 16.4K.

Shoebill Finance – a non-custodial lending protocol built on Manta Pacific.

Lenders deposit funds into Shoebill Finance and receive interest payments from borrowers (supply-side fees). They currently take a cut of the total interest paid by borrowers (revenue).

- Since launching in December '23, Shoebill's total active loans on Manta Pacific climbed to a peak of $52.4M on January 21st.

- In January '24, Shoebill generated a total of $88.1K in fees, of which the protocol captured 50%, so $44.1K, in revenue.

New metrics

We recently introduced two new metrics:

AFPU and ARPU work as simple measures of how efficiently a project is making money. They are important metrics used to understand profitability and growth potential.

We calculate AFPU/ARPU by dividing the project's daily fees and revenue by the number of daily active users.

High values indicate high fee or revenue contributions relative to the number of users. Low values suggest that most users are generating little fees.

Why AFPU and ARPU are important for investors and builders

Investors and builders can utilize these new metrics in several ways. Below are a few examples:

- Compare performance across a market sector. The metrics offer a standardized measure to assess relative performance. For example, we can look at the blockchains (L2) market sector to see which protocols generate the most daily fees per user.

- Understand a project’s ability to monetize its users. The metrics provide a starting point to analyze a protocol's financial efficiency and unit economics. For example, we can look at Curve's ARPU, which is consistently over $20. This is higher than most within the DEX market sector and demonstrates Curve's ability to effectively monetize its user base.

- Identify growth opportunities. Rising AFPU/ARPU metrics indicate a project's ability to increase fees/revenue from its existing user base. By looking at the DLN dashboard, we can see an upward trend in daily AFPU. This could mean that existing users are willing to pay more for the cross-chain trading services offered by DLN. Alternatively, DLN could be attracting mercenary users related to airdrop speculation. Context is important when assessing the sustainability of an observed trend.

For project teams

Support for strategic decision-making: Understanding AFPU/ARPU can guide strategic decisions, such as which markets to enter, which products to develop, or how to price products/services.

User value assessment: AFPU/ARPU provide insights into the value of a customer base. A higher AFPU/ARPU often indicates a more valuable customer segment, which can influence marketing and product development strategies.

For investors

Analyze a project’s pricing power: A consistently high or increasing AFPU/ARPU can be a sign of strong pricing power. It suggests that users see value in the products or services and are willing to pay more, which is a positive sign for long-term profitability.

Assess the impact of business strategies: By observing how AFPU/ARPU changes in response to new business strategies, product launches, or pricing changes, investors can gauge the effectiveness of a DAO's or management team's decisions.

Identify growth potential: Changes in AFPU/ARPU over time can indicate growth potential. For instance, if a project is increasing its AFPU/ARPU, it might be successfully upselling or cross-selling additional products and services to existing users.

👓 Insights from Token Terminal research

State of the Liquid staking market sector

The aggregated value of assets staked within the liquid staking market sector, accounting for projects listed on Token Terminal, is up 53% over the past 180 days. During this period, the price of ETH increased by 19.2%, and e.g. SOL surged by 235%. Accounting for these and other asset price changes, the actual growth in newly staked assets is ~28%. Market leaders, Lido and Coinbase, have collectively seen a 17.45% increase in new ETH staked, with Lido at 18.1% and Coinbase at 22.2%.

Excluding Lido and Coinbase, which together hold more than 80% of the total assets in the liquid staking market, we can see that the smaller LST providers have shown significant growth. Over the past 180 days, there has been an 84.5% increase in net new assets staked within this emerging segment.

EigenLayer, a liquid restaking provider, has rapidly emerged as a notable player in the market. Restaking is becoming an increasingly significant segment, driving growth throughout the whole ETH liquid staking market. It's important to note that restaking involves staking LSTs, which results in a "doublecount" of the underlying ETH in liquid staking protocols when looking at the total amount of assets staked across the market. For more granular analysis, it is worth seperating liquid staking from liquid restaking, as they differ in terms of comparability.

The amount of LSTs that have been restaked on EigenLayer has skyrocketed by 950% in the last six months. Removing EigenLayer from the equation, the amount of assets staked across the emerging LST providers has increased by 60% over the past 180 days. Relatively speaking, the longtail of LSTs is growing 2.5x faster than market leaders Lido and Coinbase.

Find a more detailed overview of EigenLayer in the 'Data Room' section of this article.

The rise of Solana LSTs

Liquid staking on Solana has seen a significant uptick. Accounting for the 258% rise in the price of SOL over the past 180 days, the net new SOL staked on Marinade and Jito over the same period are up 60.6% and 407.5% respectively.

This growth is fueled by the 'resurgence' of the Solana ecosystem, and attractive incentive programs. Marinade's Earn program, now in its second season, rewards stakers with 1 MNDE for every 2 SOL staked. Meanwhile, Jito adopted a retroactive approach, distributing JTO tokens via a December '23 airdrop.

Despite their different incentive structures, both providers have successfully maintained the growth in staked assets. This underscores the evolving nature of incentive mechanism design in crypto. As discussed in the latest Analyst Coverage episode, delving into the detailed data on the effects of different incentive programs is crucial for crypto teams aiming to build long-term, sustainable communities and businesses.

Institutional-grade staking: Liquid Collective

Increased interest in staking solutions tailored for institutions. Liquid Collective, launched in March '23, is a liquid staking solution designed to serve the needs of enterprises and institutions. It provides features such as top-tier Ethereum Node Operators, staking performance Service Level Agreements (SLAs), built-in slashing coverage for all holders, and a design focused on regulatory compliance. In September '23, Liquid Collective joined the ranks of Ethereum's top 10 liquid staking protocols and has since reached a total of $80M in assets staked.

Strategic developments fueling growth. Liquid Collective's growth is being driven by strategic advancements including making the protocol’s source code public, Twinstake joining Liquid Collective as an Integrator, and Liquid Collective’s Node Operator working group announcing its initiative to develop the Ethereum ecosystem’s first open validator performance and security standards. Restaking support for LsETH will be going live on EigenLayer this month with an open deposit window from Jan 29 - Feb 2. We expect this to even further drive growth, in a similar way to what we've seen with ether.fi.

The steady growth of Liquid Collective suggests a market trend towards institutional-grade solutions in DeFi. The platform's approach combines decentralized development with technology that adheres to enterprise compliance standards, positioning them well to capture increasing institutional demand.

📂 Data Room

Handpicked insights from the Token Terminal Data Room

A deep dive into EigenLayer

EigenLayer, built on Ethereum, introduced a novel cryptoeconomic concept known as restaking. Restaking allows users to repurpose staked ETH for validating EigenLayer's smart contracts. This is crucial because Ethereum cannot validate off-chain transactions, creating a security gap for apps that require off-chain transactions.

EigenLayer's solution involves using restaked assets to validate these off-chain transactions via its Actively Validated Services (AVS). This enables ETH stakers to enhance the security of multiple services at once, simultaneously increasing capital efficiency and trust guarantees to individual services. Restakers earn rewards from the network fees generated by these services.

Actively Validated Services (AVS)

Any system that requires its own distributed validation semantics for verification, such as sidechains, data availability layers, new virtual machines, keeper networks, oracle networks, bridges, threshold cryptography schemes, and trusted execution environments.

Source: https://docs.eigenlayer.xyz/overview/key-terms

EigenLayer enables LST holders to participate in operating offchain distributed systems. The above chart illustrates the dollar amounts of various LST tokens staked on EigenLayer, spanning from June 2023 to January '24. Notably, the red arrows mark the precise dates (12.7. & 22.8.2023) when staking limits were removed.

stETH holders are currently placing the most economic trust in EigenLayer. Economic trust refers to a trust model where validators' commitments are financially backed, creating a secure system where breaking rules leads to substantial financial penalties. Leading the way are holders of Lido's stETH token, who have collectively staked approximately $450M with EigenLayer. This is followed by Swell's swETH tokenholders, with around $270M staked.

The popularity of EigenLayer's restaking service stems from the opportunity to earn future rewards through AVS. This appeal is further enhanced by EigenLayer current points incentives for deposits. A key motivation for EigenLayer to boost staked asset volumes lies in enhancing the economic trust provided by AVS, a crucial aspect of the three dimensions of programmable trust and a central element of EigenLayer's product offering.

The above further illustrates the depth of trust individual depositors place in EigenLayer per LST, also serving as a proxy for airdrop farming trends. Depositors of Stader Labs' ETHx lead with an average deposit size of $102K on EigenLayer. In contrast, depositors of Swell's swETH and Coinbase's cbETH are at the lower end, with averages of $5.5K and $6.9K respectively.

Over half of all unique liquid staking depositors on EigenLayer are depositing swETH. 67% of all Swell stakers have restaked their swETH through EigenLayer, leading to a total unique depositor count of 49K, significantly outnumbering other LSTs. In comparison, the runner-up, stETH, has 13K unique EigenLayer depositors.

The surge in swETH's popularity is largely attributed to incentive farming, particularly through the Swell Voyage campaign. This campaign enables participants to earn "pearls" for activities like holding swETH and providing liquidity, which are redeemable for SWELL tokens at the Token Generation Event (TGE). The high number of unique depositors in swETH suggests a strategic approach by users, possibly involving the distribution of deposits across multiple wallets to maximize potential gains in both SWELL and EigenLayer token allocations.

On January 29th, EigenLayer is set to raise its staking caps, and three new LSTs - frxETH, mETH, and LsETH - will become eligible for staking. We expect this expansion to further boost the volume of restaked assets; improving EigenLayer's product through the ability to offer stronger economic trust assumptions. Drawing a conclusion from the above charts, it's evident that users are actively optimizing yield through a combination of staking, restaking, and speculative airdrop farming. This trend is likely to continue, driving up the unique depositor counts for new, pre-token LST providers.

Raw and decoded onchain data from 14 chains, accessible via Google BigQuery. Explore our Data Room offering: https://tokenterminal.com/product/data-room

📈 Trending wallets

The Trending wallets dataset captures the activity of the top 1000 gas-consuming externally owned accounts (EOAs) across 14 ecosystems. Metrics are standardized to enable cross-chain analysis, allowing for comparative assessment of activity data at the individual account level. Key metrics include:

- Gas spent (native, USD) and Gas market share (%)

- Transactions (count)

- Successful transactions rate (%)

- First and Last transaction timestamp

- Transfers to/from (count)

- Most transfers to/ from <address>

- Most interacted contract

- Most called function

- Inflows, Outflows, and Net flows

across a range of time frames: from 24 hours to 1 year.

Explore the Trending wallets metric glossary here.

Top 15 trending wallets by 30d gas spent

JaredFromSubway.eth currently leads the Trending Wallets ranking across the top 14 ecosystems, having spent a remarkable $10.77M in gas for 152.97K successful transactions on the Ethereum network in the last month. But who exactly is behind JaredFromSubway.eth? This EOA is primarily associated with MEV Bot activities, as indicated by its most interacted contract field, particularly with the MEV Bot: 0x6b7...A80. The characteristics of bot-driven activities include exceptionally high numbers of transactions and significant gas expenditures. These traits are evidently present in the activities of JaredFromSubway.eth and its associated bot contract.

Over half of the largest gas-consuming wallets, 8 out of 15, are transacting Tether (USDT) on Tron. The majority of these wallets, 6 out of 8, are affiliated with Binance, cumulatively spending nearly $11M in gas fees for almost 6M transactions. Additionally, the next 10+ top Tron wallets predominantly transfer Tether (USDT), as evidenced by their most interacted contract. This pattern indicates that the network's activity is almost entirely driven by the stablecoin issuer and major centralized exchanges that are involved in the transfer of the dollar-pegged token, USDT.

6 of the 15 most active EOAs by gas usage are those connecting the most widely-used blockchains (L2) to Ethereum mainnet. These include Arbitrum, zkSync Era, Linea, OP Mainnet, Mantle, and Starknet. The primary contracts these accounts interact with are other Layer 2 accounts, which facilitate cross-chain communication. Notably, this communication occurs through wallets rather than contracts. This could be seen as a potentially safer architectural choice, as it avoids storing any logic in the accounts that could be exploited by malicious entities.

📣 Insights from our community

Token holders of two of the biggest L2s @Optimism and @arbitrum have been steadily growing since April and are currently approaching 2 million combined.

— The Rollup (@therollupco) January 24, 2024

Graph by @tokenterminal pic.twitter.com/8f4nlVIJDg

The number of people using onchain applications is at all time highs. 📈

— Erik (@eriksx) January 24, 2024

via @tokenterminal pic.twitter.com/sRvbTNSHYp

Explore Terminal Pro: https://tokenterminal.com/product/pro

ICYMI

Analyst coverage™ of zkSync

Explore the Terminal: https://tokenterminal.com/terminal

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

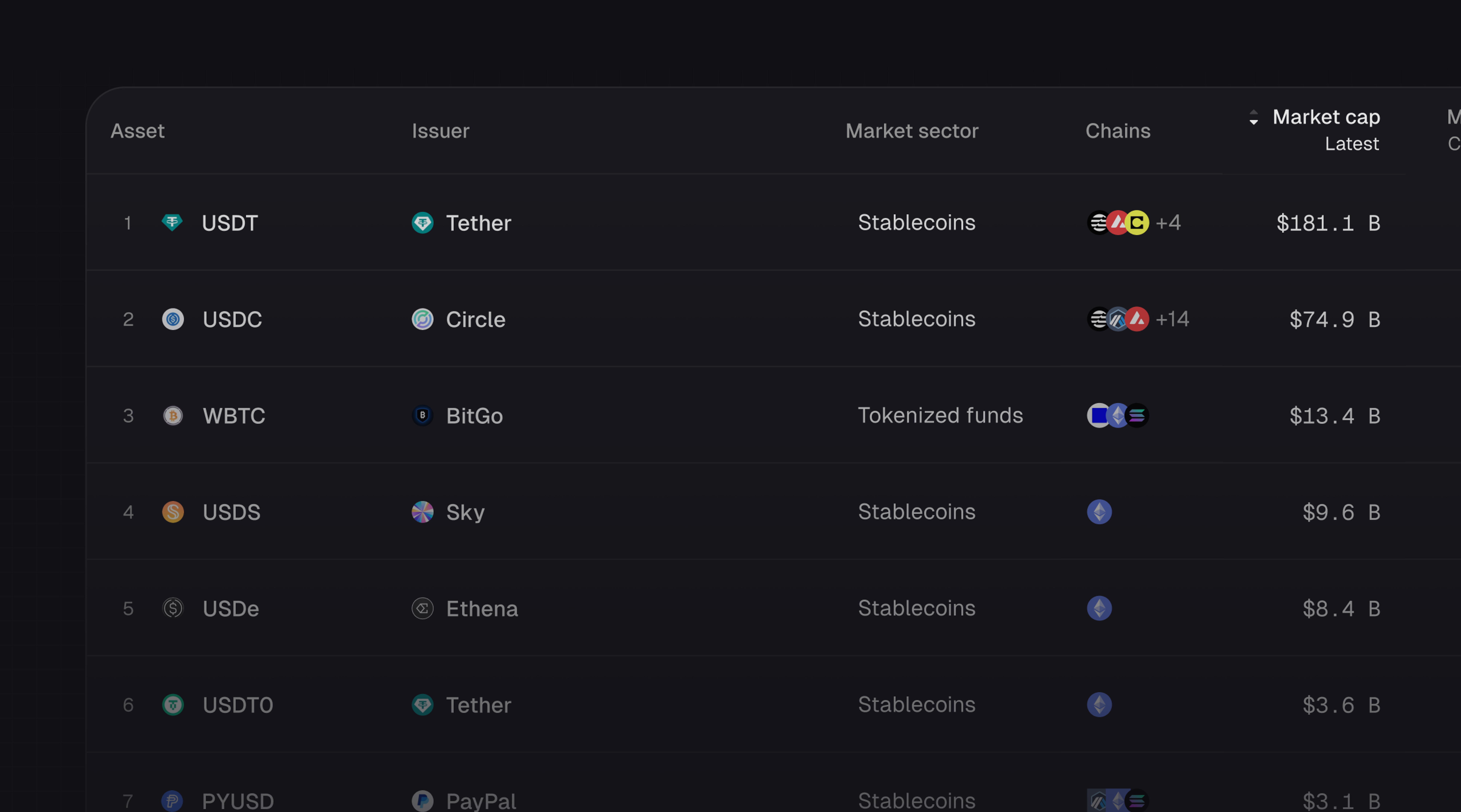

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.