Research

TL;DR: Opyn is a smart contract based insurance platform built on the Convexity Protocol.

Token Terminal

•

TL;DR: Opyn is a smart contract based insurance platform built on the Convexity Protocol. Opyn provides a well-needed and extensive insurance solution for the quickly growing DeFi ecosystem.

What problem is Opyn solving?

As the DeFi space grows, it is clear that better insurance coverage is needed.

DeFi insurance solutions should consider all possible attack vectors: technical, financial and admin.

Opyn’s options-based insurance does that.

How does Opyn provide DeFi users access to insurance?

Opyn has built an insurance platform on top of a generalized (supports both put and call) options protocol called Convexity.

Opyn’s insurance is based on the use of protective put option strategies.

Why is now the time for DeFi insurance?

To date, a non-trivial amount of ETH ($1 billion) has been locked in different DeFi protocols.

In anticipation of future growth, both builders and investors require insurance to provide security against hacks and liquidity crises.

How big is the market for options trading?

In traditional finance, options have an annual exchange volume of more than $635 trillion (excluding OTC trades).

There’s plenty of room for growth.

Who are Opyn’s competitors?

To date, mutual-style (e.g. Nexus Mutual) insurance.

Problem: mutuals have complicated governance regarding the payouts of insurance claims.

Options-based insurance provides cover regardless of the reason, if the price of the insured asset drops.

What are initial use cases for Opyn’s insurance?

Insurance for DAI and USDC deposits on Compound. Opyn recently added support for ETH.

Going forward, the team is exploring to add support for new collateral types: ERC-20 tokens, interest-bearing assets to minimize the opportunity cost for option sellers, etc.

How do you insure e.g. DAI?

Assume someone wants to buy (option buyer) and sell (option seller) insurance against the value depreciation of DAI.

The option seller locks up ETH in a vault to mint option tokens (oTokens).

Then, the option seller defines the parameters for the oTokens.

oTokens with same parameters make up a fungible oToken series, which aggregates liquidity as more similar oTokens are minted.

Once oTokens have been minted, the option seller can sell them on the open market to obtain premiums.

Their prices serve as on-chain oracles for volatility and risk in DeFi.

For example, a price increase for a protective put on DAI may indicate a vulnerability in MakerDAO.

DAI:USDC put option buyer can sell DAI for $0.99 USDC until the oTokens expire.

If the value of DAI drops below $0.99 USDC → oTokens become valuable for the buyer.

Profit: $0.99 USDCI — price of DAI * # of oTokens.

Profit is paid from option seller’s collateral.

How is Opyn governed?

Opyn is currently owned and administered by core team and early investors.

Admins update oToken parameters, manage whitelist of oTokens and set names/symbols for oTokens — protocol is noncustodial.

No native token, yet.

Path to decentralization: Opyn — or the underlying Convexity Protocol — should eventually move to community-governance à la Compound.

Eventually, the owners should want to find a way to distribute a part of the insurance premiums to Opyn tokenholders.

Token Terminal provides financial and business metrics on crypto protocols — metrics we’re used to seeing applied to traditional companies, e.g the P/E ratio. Crypto protocols operate like traditional businesses, only they do it directly on the Internet.

For more, check out Token Terminal’s website and Twitter.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

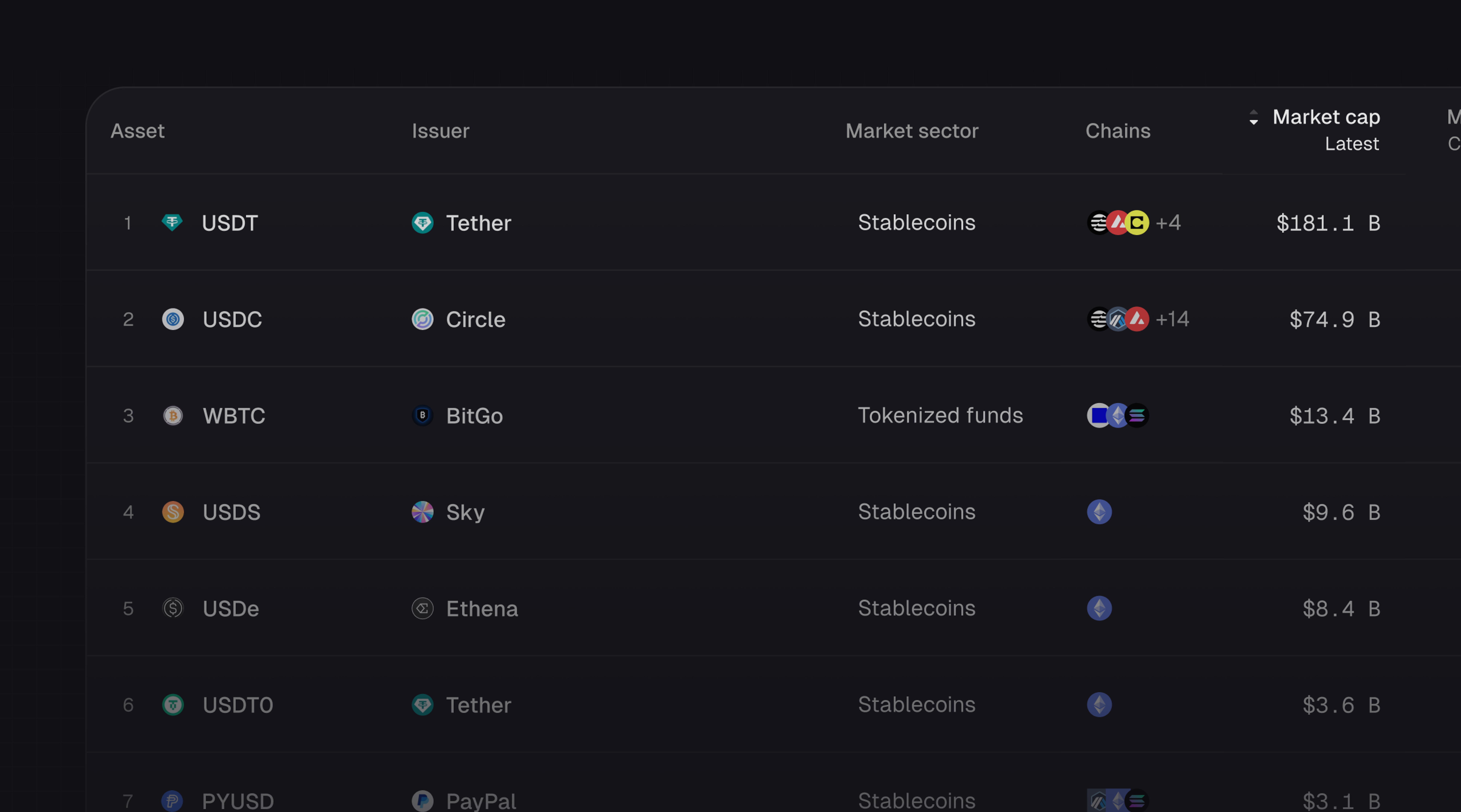

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.