Research

The cash flows of a protocol are eventually directed to its token holders

Token Terminal

•

As we’ve outlined before, the majority of the leading crypto protocols (blockchains and decentralised applications) function like marketplace businesses.

Let’s unpack what this means. 👇

How do crypto protocols work?

At a high-level:

- They provide a service

- Charge a fee for it, and

- Distribute the fees between the stakeholders, i.e. supply-side participants and token holders

Even if a protocol initially operates without a revenue share ( = the supply-side participants get to keep 100% of the fees generated), it doesn’t mean that one couldn’t be activated once the service has grown defensible enough.

In other words, as long as a protocol has paying users, turning its token from an unproductive to a productive asset depends only on the token holders' decision to activate a revenue share, and thereby direct a part of the fees from users to the protocol, rather than its supply-side participants.

Let’s go through a few examples to illustrate this point better.

BTC is still unproductive, whereas ETH isn’t anymore

On November 12th, the Bitcoin blockchain generated $981,839.65 in transaction fees, all of which were paid to the miners.

If you look at Bitcoin as a static system, you can argue that BTC the asset is purely speculative and unproductive, as it does not accrue a share of the transaction fee revenue.

Fortunately, we can already point to another blockchain, namely Ethereum, where its token evolved from non-productive to income-generating through a governance process that activated a revenue share between the miners and ETH holders. 👇

On November 12th, the Ethereum blockchain generated $70,246,289.66 in transaction fees, of which $6,685,104.34 were paid to miners, and the rest $63,561,185.32 were burned and thereby distributed to ETH holders (the burn mechanism functions similar to a share buyback).

If you look at Ethereum as a dynamic system, you can see how ETH the asset evolved from unproductive to productive, as it now does accrue a share of the transaction fee revenue.

UNI is still unproductive, whereas SUSHI isn’t anymore

On November 12th, the decentralised exchange Uniswap generated $6,651.894.76 in trading fees, all of which were paid to liquidity providers.

If you look at Uniswap as a static system, you can argue that UNI the asset is purely speculative and unproductive, as it does not accrue a share of the trading fee revenue.

Fortunately, we can already point to another decentralised exchange, namely SushiSwap, where its token evolved from non-productive to income-generating through a governance process that activated a revenue share between liquidity providers and SUSHI holders. 👇

On November 12th, the decentralised exchange SushiSwap generated $1,493,064.30 in trading fees, of which $1,244,220.25 were paid to liquidity providers, and the rest $248,844.05 were distributed to SUSHI holders.

If you look at SushiSwap as a dynamic system, you can see how SUSHI the asset evolved from unproductive to productive, as it now does accrue a share of the trading fee revenue.

In summary

Even if many protocols are initially bootstrapped through the use of token incentives or liquidity mining, there’s nothing fundamentally speculative or unproductive about how crypto protocols work.

As long as a protocol has paying users, the only thing that keeps its token from being productive is if the token holders haven’t yet decided to activate a revenue share vs. the supply-side participants.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

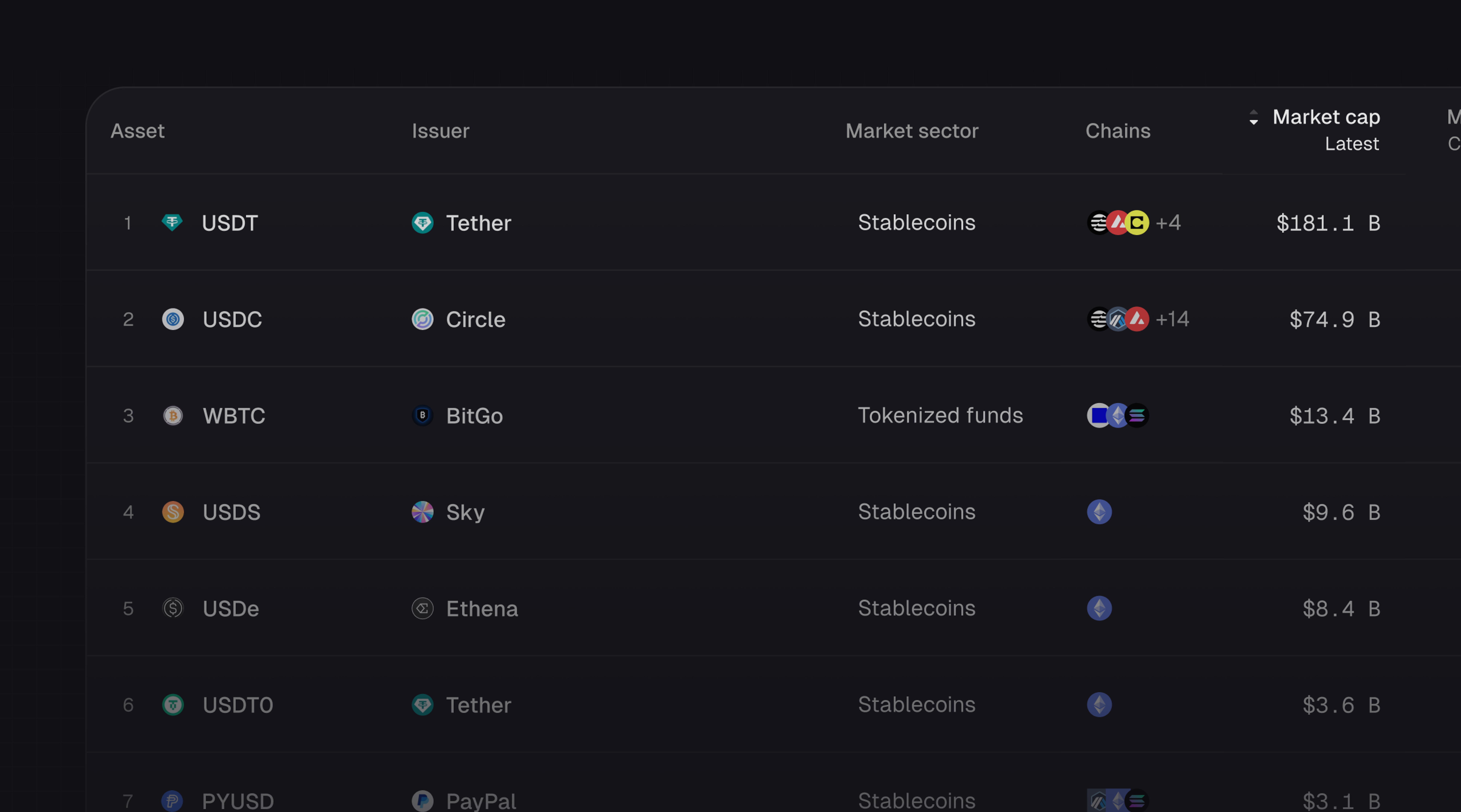

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.