Interview

The state of Euler

Token Terminal

•

In this series, we interview core protocol contributors & together dive into the details behind the charts available on Token Terminal.

Watch the full interview on YouTube, listen to the audio version on any podcast platform, or read the write-up below.

Below is a write-up of our discussion about the current state of Euler Finance with Co-Founder & CEO Michael Bentley (edited for clarity).

This interview was recorded on May 5th. Some information has been updated to reflect the current state of Euler Finance.

Q: Could you give a quick intro to Euler Finance for those not yet familiar?

Euler is a DeFi lending and borrowing protocol on the Ethereum network. It allows users to deposit ERC20 tokens into the protocol and lend those out to borrowers. Like most other lending and borrowing protocols in DeFi, it’s overcollateralized lending. Borrowers that take assets out of the protocol have to put more value in as collateral before they can take assets out. The majority of lenders tend to be people seeking to earn passive income from their assets, while borrowers tend to be more active and advanced DeFi users. These advanced users are typically able to generate profits from their borrowing activities, of which they then pay a portion back to the lenders.

Q: What are the main differentiators between Euler and other lending protocols?

We have a lot of differentiators, and I would advise anyone reading this to check out our whitepaper for a more detailed answer.

When we first developed the Euler protocol, we were looking at how other lending protocols like Compound and Aave were only listing a small number of assets. They were in some way acting as gatekeepers to what people could lend or borrow on Ethereum. One of the key differentiators with Euler is allowing users to borrow almost any ERC20 token — so allowing the permissionless listing of assets. We are able to do this because we build on top of Uniswap v3 as a core oracle protocol. This enables users to activate their own markets and manage their lending and borrowing facilities.

However, the fact that we support the long tail of assets is not even our biggest feature. The one I’m most proud of developing is the way that we manage risks and improve capital efficiency relative to other lending protocols. The liquidation engine on Euler works in a way that borrowers who get liquidated end up paying a lot less in bonuses to the liquidators than they would elsewhere. This is important because large borrowers on Compound and Aave, who are taking out millions of dollars worth of loans, don't want to be paying a five or ten percent bonus from their collateral to liquidators if they were to be liquidated. To prevent this, they'll typically overcollateralize a lot more which ultimately lowers capital efficiency across those protocols and the wider DeFi ecosystem that depends on them. Euler reduces the bonus that's paid by these users, which massively increases capital efficiency on the protocol.

Finally, it's worth highlighting that we were one of the first protocols to innovate on the way interest rates are set in lending protocols. We have a reactive interest rate mechanism which is now talked about a lot in DeFi. We actually developed this a couple of years back as a way to set interest rates in a decentralized way, using something called control theory.

Q: Can you break down your protocol revenue and your approach to managing the protocol's reserves?

How overcollateralized lending protocols typically work is that they take a portion of the interest paid by borrowers, and rather than hand that back to lenders they'll keep it within the protocol. The primary purpose of these so-called reserves is to backstop the protocol’s lenders.

From time to time some people will end up in a position where they can't repay their debts, which leads to something called bad debt. If bad debt spreads too much, lenders tend to get nervous that they might be left holding a bag of bad debt when they want to withdraw their assets. This nervousness leads to withdrawals, which ultimately leads to a spiral where lenders are front-running one another to withdraw, and you end up with a bank run in your hands. So the primary purpose of reserves is to be there to grow faster than bad debt accumulates on a protocol. On Euler, we think it's really important to generate reserves at the start when the protocol is in its infancy. This way you can accommodate more lenders.

Say you're a lender wanting to deposit 100 million into Euler today and you see there's no reserves. This might make you nervous that you’d end up holding some bad debt in six months time. The more you can accumulate reserves, the more a lending protocol can accommodate lending, so you get these kind of cycling effects.

On Euler we do a few things differently to Compound and Aave with respect to how reserves grow and work. Reserves on Euler are perpetually reinvested back into the protocol so they earn compound interest and grow exponentially over time. Whilst the protocol is in its growing phases, we set a higher reserve factor on Euler which means that roughly a quarter of the interest paid actually goes back to the protocol and not back to the lenders. Obviously this comes with trade-offs. On one hand, the more you give back to lenders, the more they come to the protocol. While on the other hand you have this problem with lenders being nervous about bank runs and things. There's definitely a sweet spot that protocols try to hit.

There's also another mechanism on Euler that tops up reserves through liquidations. Because of the aforementioned method we use to set the liquidation bonus, which works through a dutch auction mechanism, we allow liquidators to repay more of a loan than they actually need to. If a liquidator needed to pay 100 USD worth of USDC, they'll actually end up paying 102 USD worth of USDC on the loaned asset. These two extra dollars go to the protocol’s reserves. This means that when the market's turbulent and liquidations are flying around, the most volatile assets on the market that are triggering those liquidations actually see their reserves growing faster than the reserves of more stable assets. Thus lenders can be more confident about lending in the future. If you're lending something that's volatile, you should be more nervous about being left holding some bad debt at some point.

These are the two mechanisms by which our protocol reserves grow, hopefully exponentially, so that we can accommodate more lending in the future.

Q: After moderate growth during the first few months after launch, you picked up some speed around March 2022. Can you explain the drivers behind this?

When we launched back in December, we wanted to do so in a really risk-averse mode. I know that it's popular to launch a protocol to great fanfare and have people apeing in, but we didn't want that. There's lots of risks involved at the early stages and we didn't want to expose anybody using Euler to this. We launched with only three collateral assets and required everyone to overcollateralize by 4x on launch. Clearly this is not the kind of capital efficiency that you'd expect and hope to see from a DeFi protocol, but that was there to keep users safe. As we approached the new year, we started to demonstrate how governance proposals might work in the future to relax some of the constraints set on the protocol to improve capital efficiency and allow more borrowing. We started to illustrate how a proposal looks like to promote an asset to a collateral tier (we'll talk about these different tiers later), and added new collateral assets including wBTC, UNI, and LINK. There will presumably be more assets added as collateral types in the future.

We also started to relax some of the aggressive constraints we placed on capital efficiency, allowing people to borrow against their assets with a lot lower collateral ratios. This has definitely been driving our growth.

Another aspect is that we will soon be launching a governance token, EUL, that will help manage the protocol and its governance. We’ve already started allocating EUL to users of the protocol through a distribution scheme in March, once we'd grown confident enough that the protocol was working as intended. Currently, you'll receive a distribution of EUL if you're borrowing on some of the key markets on the protocol. While the main purpose of the token is to distribute it back to ordinary users, these things tend to have a stimulating effect on some markets, which we probably see on the charts as well.

Q: What is the current status of the EUL token launch and your transition to decentralized governance?

We were hoping to have it out about now, but of course it takes a little time to set these things up in the background. One thing that's been underway is the establishment of an Euler foundation. Its purpose will be to aid the DAO in future activities. If the DAO wants to e.g. distribute a grant to somebody to work on the protocol, the foundation will be there as a public face to represent the DAO in these contractual agreements. We're seeing that the foundation model is quite popular within DeFi, and we felt that it's a good model to take on board. We're hopeful that we'll be able to unlock the token and start decentralizing things in the coming months. It will be a process of progressive decentralization, and unfortunately we will be relying on the old multi-sig to control things for a little while longer.

In the long run, I've been impressed with the way Compound progressed their decentralization and we'll most likely follow a similar model to that. I estimate the transition to full decentralization to happen sometime this year.

Q: The composition of your borrowing volume is similar to what we'd see on other lending protocols like Compound and Aave, where stablecoins and wETH make up the bulk of it. What are your thoughts on the similarity here and are you seeing demand for lending and borrowing the long tail of crypto assets?

In general we'll always see a heavy bias towards the top five assets by market cap. These assets make up something like 60% of the total volume that you're likely to see anyway so there will always be an exponential distribution there in terms of volume on a lending protocol.

In terms of demand for lending and borrowing the long tail of cryptoassets, I’m frankly not sure that there's massive demand yet. There are a few reasons for this: Firstly, a protocol hasn't existed that enables this in a capital efficient way before, so the market is in quite an immature state. Secondly, a lot of the advanced users who tend to borrow assets are using these assets for leverage. Leveraging longer tail assets is much harder and it requires less capital efficiency. A lot of these traders aren't doing this yet.

On Euler you can natively long or short assets, which I know plenty of people still don't realize. We even have a quick action menu for this functionality that people can use. In the long run this might become more popular as users start to experiment with it. However, I don't think you'll ever see the same demand for lending and borrowing the long tail of assets, as they’re very volatile by nature and sometimes more illiquid which lowers capital efficiency. The use cases are also more niche, resulting in less demand. Whilst Euler offers the functionality, it's not our reason for being. It's nice to support that for more philosophical reasons; being a permissionless protocol and wanting to support a decentralized ecosystem. If you're a lender, e.g. a retail trader, and you hold a basket of five to ten assets, you have the option to hunt around DeFi and try to find homes for each of those assets to try to and earn yield. In the long run, you’ll be able to come to Euler and do all that in one place.

Like a lot of companies in the world of traditional finance will try to encourage users by offering home insurance, car insurance, banking, etc., I can see Euler becoming a one-stop-shop. There are auxiliary benefits to having long-tail assets without there being enormous demand for e.g. shorting the MKR token.

Q: How are you managing risk?

There’s lots of different mechanisms in place and tweaks to the classic model that enable risk to be managed on Euler. One of the simplest things that we implemented right from the start was the concept of a borrow factor. If you're lending and borrowing on Compound or Aave and you deposit e.g. USDC, you have two options: you can borrow some DAI, or borrow something more volatile like LINK. Your borrowing power is determined by what you've deposited as collateral, not by what you're borrowing. This doesn't really make much sense because the DAI to USDC loan is much less risky than the LINK to USDC loan. LINK can obviously go up or down in price quickly, exposing lenders to risk. The collateralization ratios for those two different types of assets should depend not just on what you're using as collateral, but also what you're borrowing. By introducing borrow factors that account for that volatility on the borrowing side as well, you can raise capital efficiency across the entire protocol.

On Compound for instance, the collateral factors of every asset are somewhat constrained by the protocol’s most volatile asset. This being the lowest common denominator which helps determine what the highest collateral factor can be even for something like USDC. Introducing borrow factors is something I think every protocol needs to do if they're supporting a variety of different types of assets from collateral to illiquid, which is what we’ve done at Euler.

We also have asset tiers which determine what you can do with different assets. Collateral tier assets are available for ordinary lending and borrowing, cross-borrowing, and they can be used as collateral. Cross tier assets are available for ordinary lending and borrowing, and cannot be used as collateral to borrow other assets, but they can be borrowed alongside other assets. And finally we have the least risky tier which is the isolated tier. Isolated tier assets are available for ordinary lending and borrowing, but they cannot be used as collateral to borrow other assets, and they can only be borrowed in isolation. If you take out a borrow of LINK (isolated tier), you can use any type of collateral you want but you can only borrow LINK from that one account. This helps protect lenders from the risks of liquidations firing off on people's accounts and leaving some markets with bad debt.

Being able to only borrow one asset from one account would be a bit painful, and would result in users having to create new accounts and move collateral between them. To solve this, we invented a system to have sub accounts generated from a single Ethereum address, so users can deposit collateral to a single address and isolated margin trade using the sub accounts that are native to that address on chain. Much like you can do isolated margin trading on e.g. Binance, you can now do that in DeFi through Euler in an overcollateralized way. These accounts are useful for risk management. If you want to take out multiple borrows — even if they're not forced to be separate from one another — you might want to do so because it's prudent to separate the collateral for different types of loans.

Q: What’s next for Euler?

Some of the things we’re working on at the moment include thinking about support for different oracle types, and support for Layer 2s and other networks. We’re also exploring integrations with other protocols. One of the things that I'm most interested in at the moment is options and the extent to which Euler could support options trading in DeFi. By combining Uniswap with something like Euler, you can generate a powerful options capability on-chain, which would be very exciting.

As we start to decentralize, we hope that other people will start contributing to this ecosystem as well.

The interview concluded.

Make sure to check out Euler Finance on Token Terminal and subscribe to our YouTube channel so you don’t miss any episodes.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

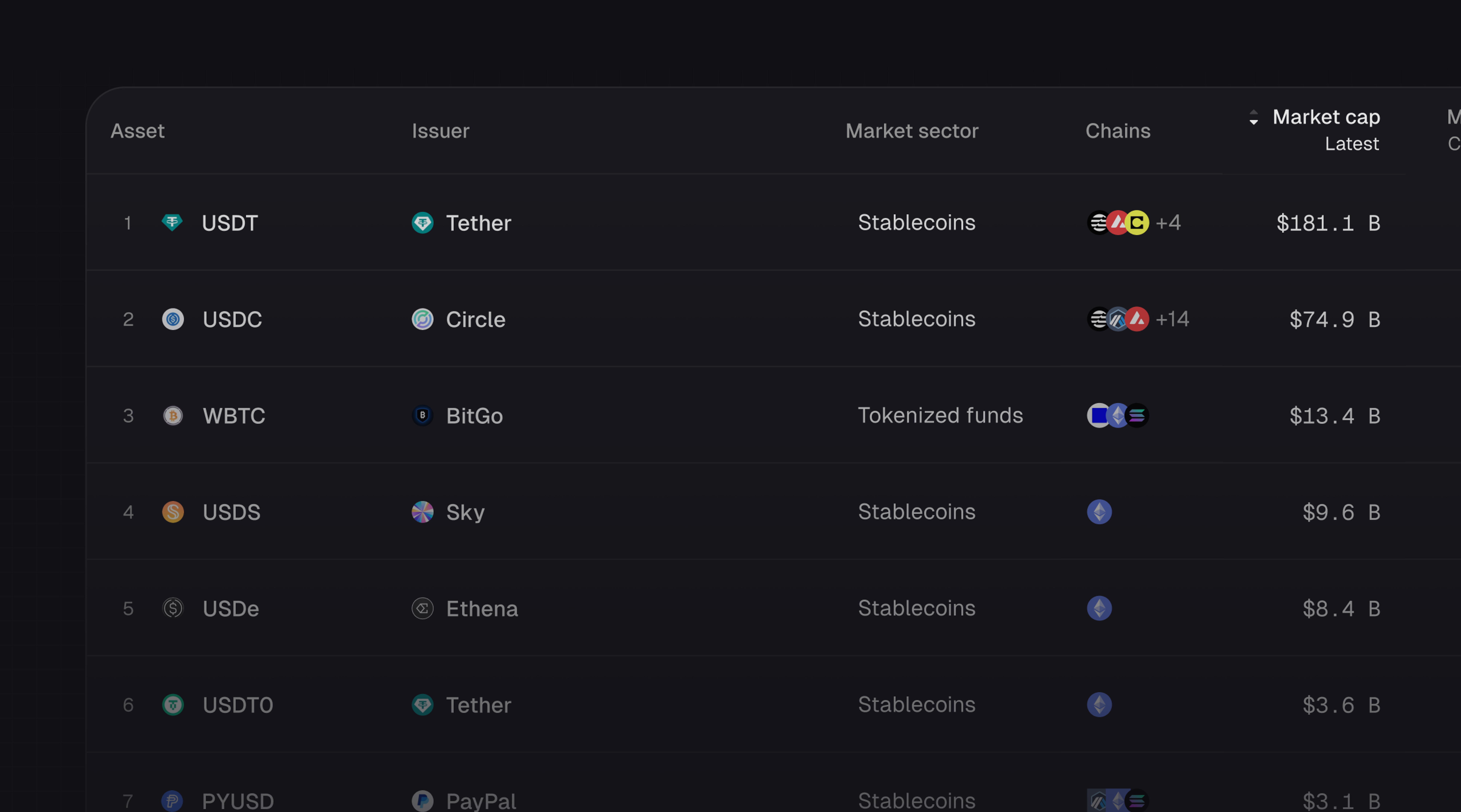

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.