Research

Research series

Token Terminal

•

This is the fourth post in our research series. In this series, we publish data-driven analysis on specific blockchains, dapps, and market segments. Let’s dig in!

Topic: Euler, a permissionless lending and borrowing protocol.

Euler is a lending protocol that allows users to borrow and lend almost any token on the Ethereum blockchain. By letting the users create lending markets in a permissionless manner, Euler is fundamentally different from established lending protocols that only support lending and borrowing of a small number of tokens. Launched in December 2021, the protocol is experiencing rapid growth and preparing to launch its governance token.

In this article, we will provide an overview of the protocol and look at its performance using Token Terminal’s data.

Protocol overview

Euler is a decentralized lending protocol whose users can lend and borrow crypto assets (i.e., tokens).

There are several established lending protocols on Ethereum, such as Aave and Compound, that support lending and borrowing of crypto assets. Users wishing to earn interest can deposit their tokens into liquidity pools where they will be made available for borrowing. However, these protocols only support lending and borrowing of tokens that have been approved by the decentralized autonomous organizations (DAO) governing the protocols. For example, less than 20 tokens can be borrowed on Compound and most of these are either stablecoins or well-known cryptocurrencies with high liquidity and market capitalizations. Lending markets (i.e., liquidity pools) for new tokens can be created through a governance process that requires a significant amount of research and administrative work. For most tokens, there are no lending markets. This is the problem Euler wants to solve.

With Euler, the creation of lending markets is permissionless. Anyone can create a new lending market by interacting with the protocol’s smart contracts. This is similar to how most decentralized exchanges, such as Uniswap, allow users to create new pools for trading tokens in a permissionless manner. However, permissionless lending markets are significantly riskier than trading pools, because a decrease in the price of an asset used as collateral can trigger a chain reaction of liquidations that affect several pools. To control this risk, Euler divides assets into three tiers: isolation-tier, cross-tier, and collateral-tier.

Assets in the isolation-tier can not be used as collateral and if a wallet has been used to borrow an isolation-tier asset, the same wallet can not be used to borrow any other assets. Cross-tier assets can not be used as collateral, but they can be borrowed simultaneously with other cross-tier or collateral-tier assets. Only collateral-tier assets can be used as collateral. By default, all assets are isolation-tier assets and their tier can be changed by governance. At the time of writing, there are 6 collateral-tier, 10 cross-tier, and 38 isolation-tier lending markets on Euler.

The basic functionality of Euler is quite similar to other lending protocols. Users wishing to earn interest can deposit their tokens into a liquidity pool and receive interest-bearing eTokens in return. These tokens can then be used to redeem the deposited assets at any time, as long as there are enough tokens in the pool that have not been borrowed. Other users can borrow tokens from the pool, given that they have deposited sufficient collateral into Euler’s smart contracts.

The value of eTokens increases over time because when loans are paid back, borrowers deposit the borrowed assets back into the pool with interest. When providing collateral, users can choose whether to make the deposited assets available to be borrowed or not. By making the assets available to be borrowed, they accrue interest but are exposed to risks of borrowers defaulting. On the other hand, by not making their collateral available to be borrowed, the risk is avoided. When calculating whether a loan is under-collateralized, Euler uses Uniswap’s time-weighted average price (TWAP) oracles to get the price of the asset in wrapped ETH (WETH). A lending market can be created for all assets that have a WETH pair on Uniswap v3. Furthermore, Euler also provides free flash loans.

The protocol is currently governed by a company called Euler XYZ who have stated stated that their long-term goal is to move towards decentralized governance using a DAO whose governance token will be EUL. The initial total supply of EUL is 27,182,818, which is an homage to the mathematical constant e = 2.71828..., known as Euler’s number. Euler was an extremely influential mathematician after whom the protocol is named. The total supply of EUL will be fixed for 4 years, after which the project governance can choose to inflate the supply by up to 2.718% per year. The figures below show the estimated distribution of the initial supply. EUL is expected to be tradeable in the first half of 2022.

Business case

DeFi lending can be a lucrative business. For example, in the past year, both Aave and Compound generated roughly 40 million USD in protocol revenue and several times more for lenders or liquidity providers. Euler’s aim is to tap into this market and expand it by enabling lending and borrowing of tokens that are not supported by other protocols. There are many tokens with market capitalizations in the billions of USD for which there are no decentralized lending markets.

By automating the process of creating lending markets, Euler could potentially scale beyond Aave and Compound. The set of all tokens includes also extremely volatile assets and scam projects. By not giving these tokens collateral-tier status, the effects of liquidations arising from these tokens’ price volatility can be limited. Other existential risks include smart contract risk and oracle risk that may result in exploits where funds are lost. Although the team behind Euler has emphasized their focus on risk management, risks are always present in DeFi.

Historical performance

In this section, we will look at Euler’s historical performance using Token Terminal’s data. For more information and to be able to interactively explore the shown data, make sure to check out our dashboard!

Since Euler is a lending protocol, let’s start by looking at the total borrowing volume, i.e., the value of outstanding loans. The figure below shows the historical borrowing volume since the launch of the protocol. After three months of consistent growth, Euler’s borrowing volume reached 50 million USD on the 22nd of March 2022, and in the following two weeks, the protocol’s borrowing volume grew six-fold, reaching 300 million USD on the 5th of April 2022.

The most borrowed token is USDC, followed by WETH, DAI, and others. To understand how relative borrowing volumes have developed over time, it helps to look at the the borrowing volume of each asset as a percentage of the total borrowing volume, shown in the figure below.

Looking at the figure above, we can see that the proportion of USDC borrowed relative to the total amount of funds borrowed has been steadily decreasing. Furthermore, over the past couple of weeks, several new borrowing markets emerged in line with Euler's goal of supporting the long tail of crypto assets.

The interest rates are automatically adjusted and vary over time and across pools, so the borrowing volume alone is not enough to know how much revenue is being generated. Let’s look at how much interest the borrowers are paying, shown in the figure below.

The figure below shows the interest paid per asset as a percentage of total interest paid. Interestingly, over 75% of Euler’s revenue comes from lending stablecoins USDC and DAI, which is quite similar to Aave and Compound, whose revenue is mostly generated from lending stablecoins.

Finally, let’s see how the revenue is split between the protocol and supply-side participants (i.e., lenders or liquidity providers). Euler charges a 23% fee from the total interest paid by borrowers.

Roadmap

After the initial development stage that led to the launch of the protocol, Euler’s focus will be on growth and community building. Euler’s governance forum was launched in February 2022 and the next big step will be the launch of the EUL token. EUL will allow the project to give out grants to developers to grow its role in the Ethereum DeFi ecosystem. However, the protocol is still in its infancy, and at the time of writing, documentation related to several governance aspects has yet to be released.

Euler has raised 8 million USD in a Series A round led by Paradigm.

Conclusion

Borrowing and lending are required features of any financial system. In DeFi, several lending protocols exist, but they only enable lending and borrowing of a very small fraction of existing tokens. Euler’s permissionless lending protocol is a genuine innovation that expands lending and borrowing to more tokens than what was previously possible.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

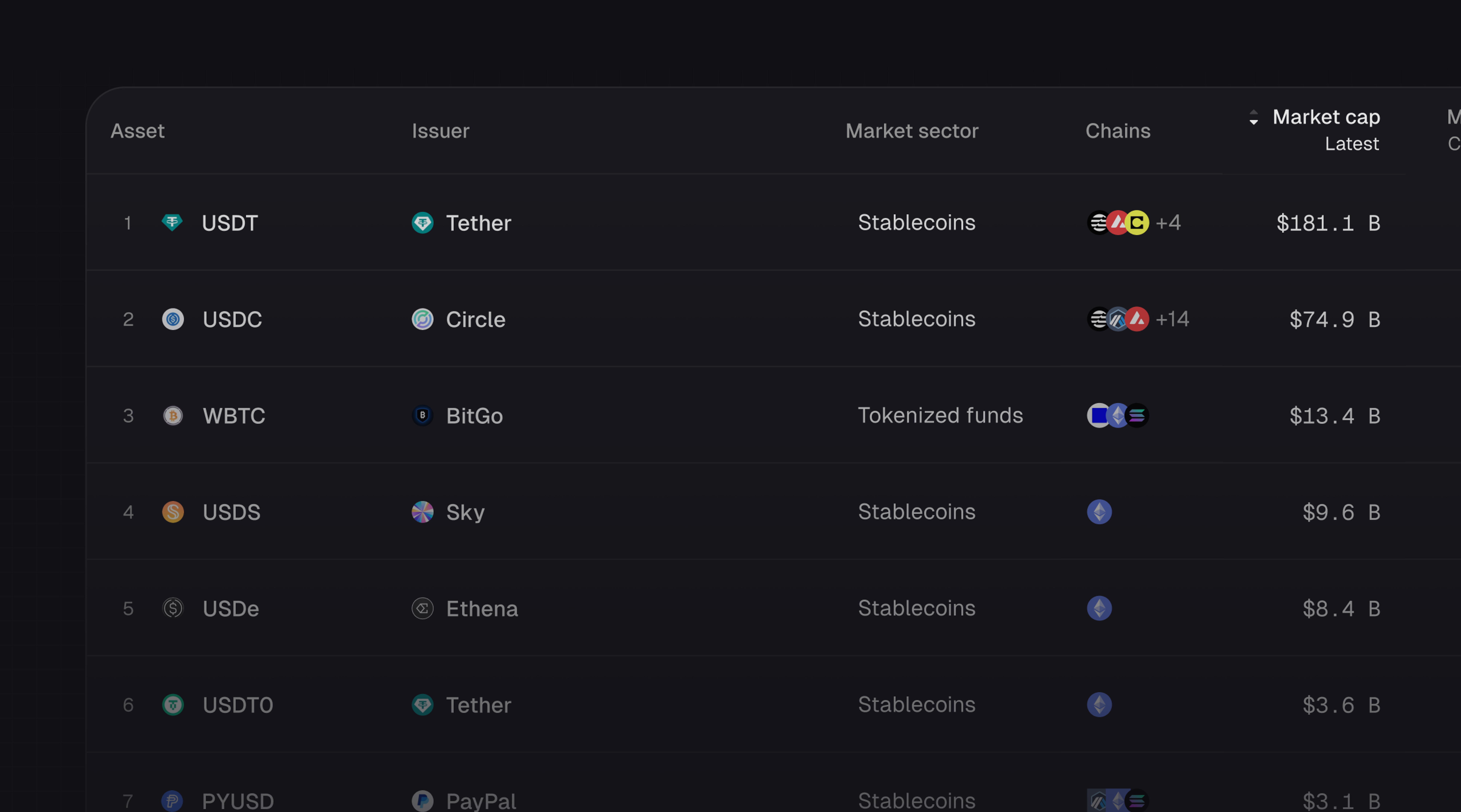

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.