Research

Research series

Token Terminal

•

Topic: Centrifuge, a bridge that allows real-world assets to be used as collateral in DeFi.

The State of Centrifuge

Centrifuge recently secured a Polkadot parachain slot with its promise to bridge the gap between real-world assets (RWAs) and decentralized finance (DeFi). It aims to provide access to cheap capital to small businesses and stable yield for investors by tokenizing RWAs such as invoices, real estate, and royalties. Their first customer-facing product, Tinlake on Ethereum, has grown significantly since its launch both in terms of total value locked (TVL) and revenue. In this short report, we will have a closer look at where the project currently stands and what the future may bring.

Protocol overview

Centrifuge enables businesses to mint non-fungible tokens (NFTs) representing verified RWAs that can then be used as collateral on loans to access capital in DeFi. This allows DeFi investors to invest in liquidity pools backed by real-world assets that can serve as a hedge against crypto market volatility.

The Centrifuge protocol consists of the following core components: peer-to-peer (P2P) messaging protocol, Centrifuge Chain, and Tinlake, highlighted in the figure below.

The P2P protocol is used to create, exchange, and verify RWA data off-chain in a private and secure manner. The documents representing the assets are stored on the P2P network and the NFTs representing asset ownership are minted on the public Centrifuge Chain. The NFTs can be bridged to Ethereum and locked into Tinlake as collateral to access financing.

Centrifuge Chain

Centrifuge Chain is a proof-of-stake blockchain built on Substrate with a bridge to Ethereum. In the future, it will connect to the Polkadot Relay Chain as a parachain to outsource its security to achieve improved security at lower cost. The chain’s native token is the Centrifuge (CFG) token, which is used to pay for transactions and whose holders can participate in governance.

The initial supply of 400 million CFG was distributed to the Centrifuge Network Foundation and initial contributors, with the majority of the tokens being initially locked. The figures below show the estimated unlock schedule and a snapshot of the token distribution in April 2021.

Currently, the annual mint rate of CFG to reward block validators and nominators is 3% of the total supply. In addition, tokens are minted to reward users of the protocol. The mint rate is controlled by governance, and according to Centrifuge, the long-term goal is to lower the mint rate if the protocol starts to sufficiently attract new users for its utility alone. The burn rate of CFG as percentage of transaction fees is controlled by governance and can be used to stabilize the number of tokens in circulation.

Tinlake

Tinlake is Centrifuge’s first decentralized application (dApp) for DeFi investors. It currently runs on Ethereum, but moving forward Tinlake will be migrated to Centrifuge Chain.

Businesses, referred to as “asset originators”, can lock their NFTs representing RWAs into Tinlake’s liquidity pools to borrow capital. Investors on the other hand, can lock USD-pegged stablecoins into Tinlake’s pools to earn yield. The investors can choose to receive either TIN or DROP tokens in return for locking their stablecoins. TIN holders receive higher yield but are exposed to more risk than DROP holders. This is similar to junior and senior tranches in traditional finance. Investors can join and leave Tinlake pools at any time.

Asset originators are required to set up a special purpose vehicle (SPV), an independent legal entity, for each pool. Investors enter into a contractual relationship with the SPV and therefore a “know your customer” (KYC) process and signing a contract are required.

Business case

Centrifuge’s goal is to connect investors with businesses in need of capital without banks or other intermediaries. According to the World Bank, small and medium enterprises (SMEs) make up 90% of the businesses and over 50% of employment worldwide. However, SMEs are less able to obtain loans from banks and have to pay higher fees than large companies. Another significant issue is the time it generally takes for payments to be received for invoices. Centrifuge uses recent innovations in DeFi, such as liquidity pools running on smart contracts, to make the process faster and more cost effective than what banks can offer.

Centrifuge can be understood to operate in asset-backed securities and factoring. Asset-backed securities are tradeable financial assets whose value is derived from underlying assets. Factoring is selling invoices and other forms of debt to other businesses. The global market size is larger than the entire current crypto market, measured in trillions of US dollars. Bringing RWAs on-chain has the potential to increase the size of crypto market by an order of magnitude. It is a lucrative opportunity and Centrifuge will compete with other crypto-native startups and large established businesses in traditional finance.

Historical performance

In this section, we will look at the historical performance of Tinlake using Token Terminal’s data. In particular, we will focus on total revenue, TVL, and valuation. Total revenue is equal to the interest paid by asset originators. TVL is the value of assets deposited into Tinlake’s smart contracts. We measure valuation using fully-diluted market capitalization, i.e. the total supply of CFG multiplied by its price.

The figure below shows Tinlake’s monthly total revenue over time. In the past year, it has grown 33% per month on average.

The number of Tinlake pools has also kept increasing as more asset originators have joined, leading to a total of 13 active pools today. From the figure below, we can see that the two largest pools (New Silver 2 and Branch Series 3) make up nearly half (44%) of the total revenue. New Silver 2 is financing a portfolio of real estate bridge loans and currently provides investors junior annual percentage yield (APY) of 15% and senior APY of 4%. Across the pools, current senior APY ranges from 3% to 10%.

Tinlake’s TVL has also grown 32% per month on average over the past year, as can be seen in the figure below.

Despite the impressive growth in terms of both TVL and revenue, Centrifuge’s valuation has not followed the same trend. In fact, CFG is currently trading at a price that is below its initial coin offering (ICO) price of $0.55. CFG’s recent price development may be explained by the significant number of tokens becoming unlocked between Q2 of 2021 and Q2 of 2022. Although, should Centrifuge continue to grow at its current pace, the trend of CFG price may reverse as the rate of newly unlocked tokens decreases and awareness of its business fundamentals increases.

When assessing the growth of the protocol, it is important to note that Centrifuge is rewarding CFG to investors in significant quantities. Currently, CFG is rewarded to investors at an annual percentage rate (APR) of 11% that is paid on top of the yield earned from the pool.

A minimum investment of $5000 and the contractual requirements to become an investor may have hindered Tinlake’s growth.

Roadmap

Centrifuge is well funded and backed by both traditional and crypto venture capital (VC) investors, giving the team significant resources to improve their product. They have raised $8M in 2018 and $4.3M in 2020. In the May 2021 ICO, they raised a further $19M by selling 42.5M CFG tokens.

The most important change in the short term will be migrating Centrifuge Chain to be a Polkadot parachain, which will enable Centrifuge Chain to get its security from the Polkadot relay chain, allowing the team to optimize Centrifuge Chain for the use case of tokenizing RWAs. Centrifuge’s goal is to also migrate Tinlake to the new parachain and provide bridges to other blockchains to access DeFi liquidity.

Another important development for Centrifuge will be collaboration with established DeFi protocols, such as the existing collaboration with MakerDAO. Centrifuge has already partnered with MakerDAO to enable DROP tokens to be used as collateral in DAI loans. Centrifuge has also created a permissioned market for RWAs using the Aave lending protocol.

Conclusion

Centrifuge aims to bring RWAs on chain in order to provide businesses fast and cheap access to DeFi liquidity, while providing DeFi investors an opportunity to invest in RWAs whose prices are not necessarily correlated with the crypto market. The project is in a good position to become one of the main players in this nascent but rapidly growing market.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

Introducing Tokenized Assets

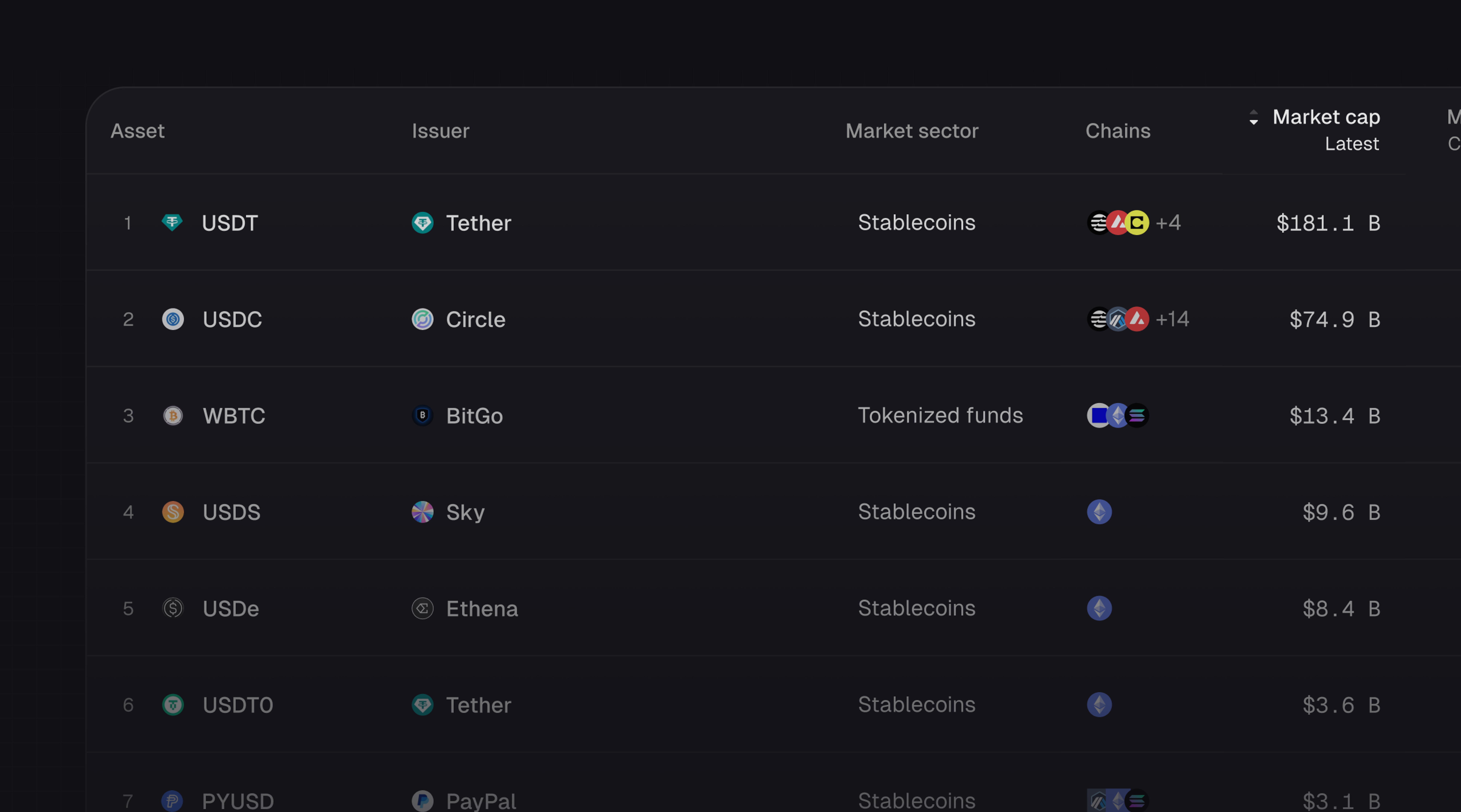

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.