Research

Nervos is a proof-of-work (PoW) L1 blockchain optimized for app-specific L2 chains. Nervos wants its native asset (CKB) to function…

Token Terminal

•

TL;DR: Nervos is a proof-of-work (PoW) L1 blockchain optimized for app-specific L2 chains. Nervos wants its native asset (CKB) to function as a more sustainable store-of-value (SoV) than BTC and its chain to function as a more secure smart contract platform than Ethereum.

Overview of Nervos

Nervos launched its mainnet in late 2019. It consists of a high-throughput L1 PoW chain.

The Nervos’ Axon SDK enables developers to run their own high-performance and Turing complete app-specific chains with custom VMs and consensus protocols.

Nervos tackles the unsustainable economic incentives of Bitcoin

Bitcoin’s capped supply (decreasing block rewards) and BTC’s role as a SoV asset (low tx activity) might lead to unsustainable economic incentives for miners in the long-run.

Nervos tackles the heavy asset dilemma of Ethereum

In Ethereum, the value of its native asset ETH is not directly tied to the value of L2 apps built on top of Ethereum.

This presents a security risk in case the value of L2 apps exceeds the value of the L1 native asset (ETH), in which case it would become economically rational to attack L1 to steal assets on L2.

Nervos has a perpetual secondary issuance for its native asset (CKB)

In addition to a base supply of 33 billion CKBs (capped similar to BTC’s 21 million), Nervos has a fixed (1.3 billion CKBs) annual secondary issuance to incentivize miners in the longer-term.

To make CKB a SoV asset, it’s used to pay for both tx fees and storage

All L2 apps need to continuously lock up CKB in proportion to the size of their app. The more demand there is for chain space on Nervos, the more valuable CKBs become.

Locked up CKBs are subject to “state rent” via inflation

Apps that lock up CKB forego the annual inflation rewards from the secondary issuance (= aka pay state rent). This model automates state rent payments.

Chain space in Nervos is subject to a secondary market

In Ethereum, data storage is paid for once and stored forever. This results in state bloat and higher requirements for full nodes. In Nervos, apps have an economic incentive to unlock and sell their CKBs if they no longer have relevant state to store.

CKB investors can offset inflation

- Investors buy CKBs.

- Deposit CKBs into NervosDAO.

- NervosDAO receives a part of the secondary issuance to offset inflation.

- CKBs in NervosDAO resemble “treasury bonds”.

Applications on top of Nervos

Nervos has set up a $30M grant to fund application development. Summa received a grant to build a BTC <> Nervos bridge similar to tBTC between Bitcoin and Ethereum. Check out the Nervos roadmap for 2020 here.

Blockchain in China is on the rise

The Nervos team has partnered with many notable investors (Sequoia China, Polychain, Dragonfly, etc.) to boost the blockchain innovation coming out of China.

Token Terminal provides financial and business metrics on crypto protocols — metrics we’re used to seeing applied to traditional companies, e.g the P/E ratio. Crypto protocols operate like traditional businesses, only they do it directly on the Internet.

For more, check out Token Terminal’s website and Twitter.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

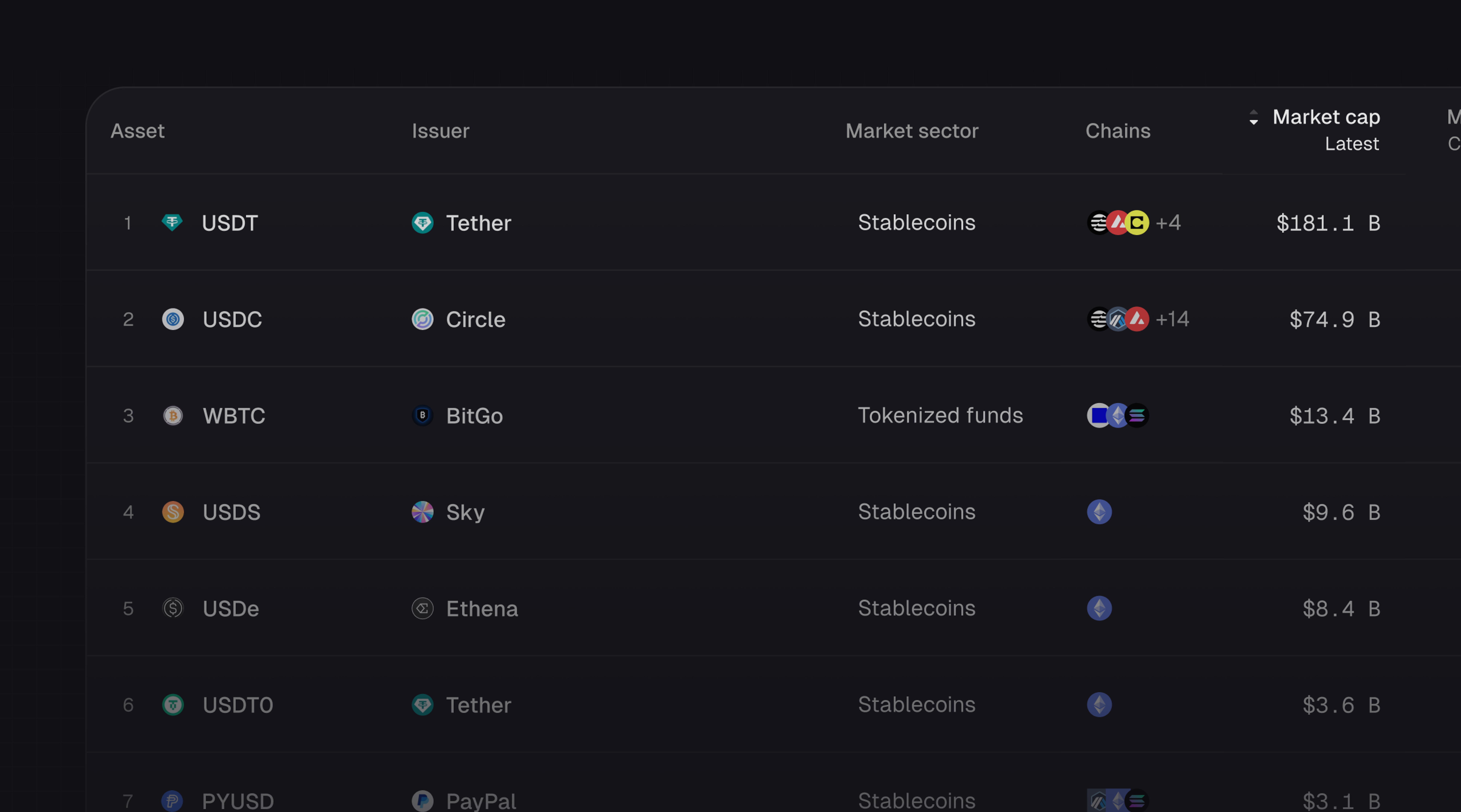

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.