Research

This article is aimed at institutional and other professional investors who are considering making an allocation to crypto.

Token Terminal

•

Executive summary

This article is aimed at institutional and other professional investors who are considering making an allocation to crypto. It examines the best practices for token investing that have been adopted by institutional investors globally. In this article, crypto investments refer to investments in tokens. The article excludes traditional equity investments made into startups that make use of blockchain technology.

An investor interested in the attractive risk-return profile of the new asset class needs to consider the additional technical and operational requirements that pertain to token investing.

The first part of the article highlights recent developments in the market infrastructure for token trading and custody. As a result, more institutional investors have been able to invest in tokens. The second part outlines the technical and operational requirements of token investing. The third part walks through the alternatives available to institutional investors interested in investing in tokens.

The development of the crypto market

The number of regulated and professional market participants is on the rise

During the early days of crypto (2009–2013), the market infrastructure for trading and custodying tokens did not meet the requirements of institutional investors. Over the past few years, a class of institutional-grade and regulated service providers has made it possible for more professional investors to enter the crypto market.

US-based Fidelity Investments is one of the leading institutional investors in the space. Fidelity is a global asset management firm founded in 1969, and serves both prominent institutions as well as high-net-worth individuals. According to a 2019 report by Fidelity, 22% of US institutional investors have made token investments over the past three years. Nearly half (47%) of the investors that took part in the survey view token investments as a part of their overall investment portfolio. Fidelity started mining Bitcoin as part of their internal R&D efforts already in 2014. Today, the firm offers token custody and trading services for their institutional clients in the US and Europe.

Examples of other well-known technology and traditional financial services firms that have made significant investments into the crypto space:

- Venture capital firm Andreessen Horowitz (a16z). In the summer of 2018, Andreessen Horowitz launched their dedicated crypto investment fund, a16z crypto (AUM $300 million). The firm raised its second crypto fund (AUM $515 million) in April 2020.

- Venture capital firm Sequoia Capital (Sequoia). In 2018, former Sequoia partner Matt Huang and Coinbase co-founder Fred Ehrsam founded the crypto investment firm Paradigm (AUM $400 million). In addition to Sequoia, the fund’s investors include Yale University endowment, whose CIO David Swensen is known for pioneering an investment strategy that emphasises alternative investments.

- Chicago Mercantile Exchange (CME). CME added bitcoin futures to their service offering in December 2017. The company introduced bitcoin options for trading in January 2020.

- The parent company of New York Stock Exchange, Intercontinental Exchange (ICE). In 2019, ICE launched the token trading and custody platform Bakkt.

Intercontinental Exchange operates its own token trading platform called Bakkt.

Today, over 20 companies that provide token custody services have obtained the status of a Qualified Custodian in accordance with New York state banking laws (New York Banking Law § 100).

Examples of regulated service providers:

Examples of regulated token trading and custody service providers.

To date, the majority of institutional investment activity in crypto has been concentrated to the US. The European Investment Fund announced at the end of 2019 its intent to allocate 400 million euros to blockchain technology investments in 2020. The mandate was given to ensure that Europe is not being left behind US and Asia in the development of leading edge technologies.

Challenges relating to the new asset class

Token ownership is a prerequisite for capturing the potential value of blockchain technology

Blockchain technology makes it possible to create and operate businesses natively on the Internet (companies registered on blockchains). In order to become an owner in these companies, an investor needs to own digital shares, better known as tokens. Traditional companies that make use of blockchain technology (e.g. Coinbase) can be funded via traditional equity investments. These companies serve as bridges between the Internet-native economy and the traditional economy. They develop market infrastructure necessary for the initial user adoption of crypto.

Traditional companies depend on the functionality of blockchain technology, and their opportunity to serve users globally is more limited than Internet-native companies’. The tokens of Internet-native companies’ resemble shares and provide their owners with both economic and governance rights.

The performance of Internet-native companies can be measured with similar financial metrics that are used to measure traditional companies. Source: Token Terminal.

Token investing takes place in an Internet-native environment

Investing in Internet-native companies (token investing) differs from venture capital investing on a few dimensions. Internet-native companies are based on open source software and they are developed primarily on the Internet — initially by a small core team and later on by a worldwide online community.

The daily development activity is concentrated to online forums such as Twitter, Discord, Medium, and Github. The transaction activity of Internet-native companies can be monitored in real time since they are based on open source and open data. In addition to transaction activity, investors need to be able to analyse the operations of their investment targets by following the development work of the core teams and the investment target’s popularity among third-party developers. Finding the relevant information and parties requires active participation in these online communities.

Examples of different Internet-native companies or token projects. Source: Token Terminal.

A professional and crypto-focused investment team is best suited to source the most promising investment targets.

Token investing in practice

The early stage of the token market favours a long-term approach combined with an active investment strategy

Token investing combines investment strategies from both venture capital and hedge fund investing, with the emphasis on the former. Even if the ownership shares of Internet-native companies are freely tradable on the Internet already during the early development stages of a project, in practice, only a small number of projects have meaningful liquidity. Venture capital investors approach the market with long-term strategies, which are not impacted by market volatility and low liquidity as much as hedge fund strategies are.

An institutional investor can choose between three different options when considering an investment into tokens: conducting the investment operations in-house, or investing either through a passively or an actively managed fund. The challenge with in-house investments stems from the requirement for internal resources, which in many cases tend to be disproportionate to the size of the token allocation. After all, token investments should make up only a small part of an institutional investor’s overall portfolio. Passive index funds (e.g. top 10 indices) tend to underperform the market, as current market inefficiencies include several low quality assets in them.

As a result, a majority of fund managers in the space have opted for a closed-end fund structure, where the investment operations are conducted with a 7+ time horizon, as is often the case for venture capital investing. Token projects today are more similar to early-stage startups than publicly listed companies, even if their tokens might have a vibrant secondary market. The early secondary market liquidity for Internet-native companies is a novelty that might make it possible for managers of closed-end venture capital funds to rebalance their portfolios during the lifetime of a fund.

Due to the untraditional investment targets and investment process, many traditional venture capital funds have exceptionally chosen to make fund-of-fund investments into other venture capital funds dedicated solely to crypto.

There are several active crypto venture capital funds operating globally.

The nascency of the crypto asset class, the regulatory questions surrounding it, and its rapid development pace, all support a long-term and active investment strategy. Blockchain technology is in many ways more akin to the Internet — a technology that had an impact on several different industries — than a single vertical, which is why a successful investment operation often requires a dedicated team.

For the reasons mentioned above, the most common form of investment in the crypto space has skewed towards dedicated crypto venture capital funds. Fund managers that operate token-focused funds tend to be younger and less experienced than their traditional counterparts.

Token Terminal provides financial and business metrics on crypto protocols — metrics we’re used to seeing applied to traditional companies, e.g the P/E ratio. Crypto protocols operate like traditional businesses, only they do it directly on the Internet.

For more, check out Token Terminal’s newsletter, website and Twitter.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

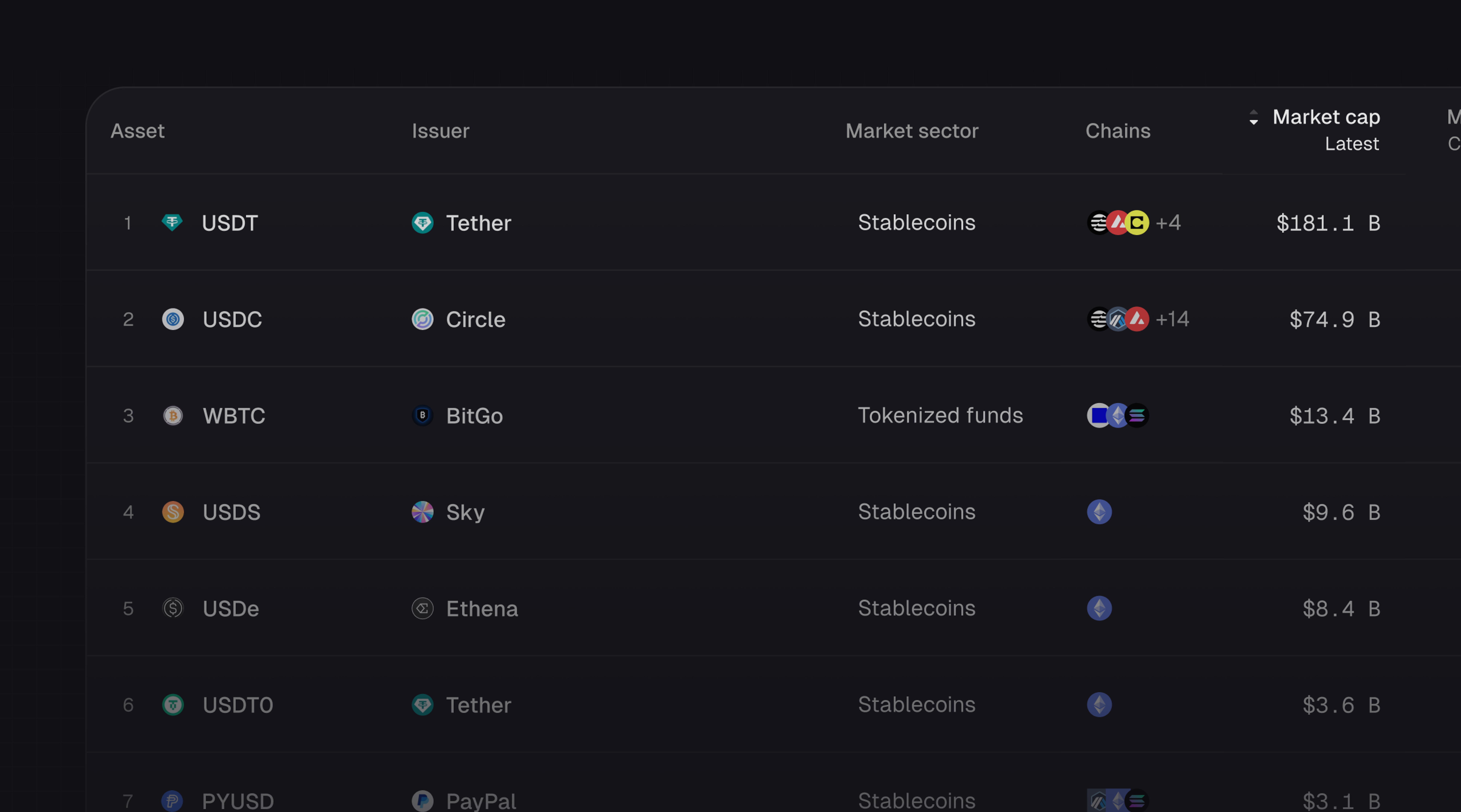

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.