Newsletter

Crypto fundamentals – charts and trends to watch

Token Terminal

•

A walkthrough of the most interesting charts and trends in crypto, with a focus on key business drivers and protocol fundamentals.

This week’s newsletter focuses on the stablecoin issuers market sector, which has a designated dashboard on Token Terminal. Let’s dig in!

Decentralized stablecoin issuers are smart contract -based credit facilities that allow users to borrow stablecoins (often pegged to the dollar or euro) against crypto or real-world collateral assets.

Overview

Below is visualized the daily outstanding supply for all projects in the stablecoin issuers market sector over the past year.

Scope of analysis

- The stablecoin issuers dashboard features 10 projects, mostly on Ethereum. Our dashboard covers ~$35 billion of the total outstanding stablecoin supply of ~$130 billion. USDT and BUSD account for ~95% of the supply not currently showcased on Token Terminal.

- Ethereum-based stablecoins represent ~50% of the total outstanding stablecoin supply, of which we cover ~50%. Notably, Vesta Finance stands out being the only project in the above chart that is primarily deployed on another chain, Arbitrum.

Centralized vs. decentralized stablecoin issuers

- Circle, Monerium, and Membrane Finance are centralized stablecoin issuers, that issue full-reserved stablecoins. These stablecoins are backed by reserves held in traditional financial institutions, with each unit of stablecoin fully backed by a unit of reserve. Decentralized stablecoins, on the other hand, are typically overcollateralized, with the value of the digital assets held by the issuer exceeding the outstanding supply.

- Centralized stablecoin issuers operate at the intersection of fiat and crypto, providing access to vast liquidity in the traditional financial system. This positioning offers significant growth opportunities, whereas decentralized stablecoin issuers are limited to the amount of high-quality collateral available within the crypto ecosystem. However, centralized stablecoin issuers are also exposed to counterparty risks from events like bank failures, despite not suffering from market risk to the same extent as decentralized stablecoins, which are often backed by volatile assets.

- It is worth noting that centralized stablecoin issuers currently operate under stricter regulations, which may limit their operations. Nevertheless, both centralized and decentralized stablecoin issuers have their own risk trade-offs, which we will cover in this newsletter.

USDC depeg

- USDC, the largest stablecoin after USDT, lost its peg to the dollar on March 10th, 2023. This can be seen on the chart as a 10% daily drop in USDC's outstanding supply.

- Circle, the issuer of USDC, had $3.3 billion in cash reserves held in the now-collapsed Silicon Valley Bank, which contributed to the loss of the peg. Also, exchanges like Binance halted USDC conversions, escalating the situation. However, after U.S. regulators announced their intention to make all SVB depositors whole, USDC regained its peg to the dollar.

- This temporary depeg created arbitrage opportunities, liquidations, and redemption issues across various platforms, leading to market volatility. The event had a significant impact on the stablecoin market and highlights the need for robust risk management strategies.

Momentum

Below are visualized some of the most interesting trends for projects in the stablecoin issuers market sector.

DAI’s stablecoin collateral

- Stablecoin collateral is backing a significant amount of outstanding DAI. Peg Stability Modules (PSM) are special vaults with USD stablecoin collateral. They have a 100% collateralization ratio and a 0% interest rate. Assets in PSM vaults are 1:1 exchangeable for DAI.

- Since PSM-USDC-A's launch in December 2020, the share of PSM collateral has grown to be the largest source of outstanding DAI. Currently, PSM-backed DAI accounts for approximately 3 billion of the 5 billion DAI in circulation.

- This liquidity helps to protect the DAI 1:1 USD peg, but at the same time, it introduces a centralization risk to the protocol. This risk was realized recently when USDC depegged from USD amidst Silicon Valley Bank's collapse. This also caused DAI to temporarily lose its 1:1 peg to USD.

RWA collateral growth

- Real World Asset (RWA) collateral in MakerDAO experiences significant growth. From August 1st, 2022, to April 23rd, 2023, MakerDAO's RWA-backed DAI experienced significant growth. Outstanding value surged from $40 million to $713 million.

- The growth has been driven by collaborations with Monetalis Clydesdale (RWA007-A), Huntingdon Valley Bank (RWA-009), and BlockTower (RWA012, RWA013).

- Monetalis Clydesdale (RWA007-A): This collaboration enables MakerDAO to invest idle PSM USDC in liquid bonds.

- Huntingdon Valley Bank (RWA-009): MakerDAO provides a DAI credit line to HVB, using the bank's assets as collateral. MakerDAO earns yield from real-world loans that HVB originates and participates in.

- BlockTower (RWA012, RWA013): Credit lines extended to BlockTower. The loans are secured with asset-backed securities and collateralized loan obligations. Centrifuge's Tinlake protocol brings these assets on-chain. MakerDAO earns interest on the borrowed funds.

- The RWA sector thrives, signaling promise for DeFi’s use cases in traditional finance. MakerDAO's DAI, backed by real assets, is growing fast. This shows DeFi's potential to further integrate with traditional finance.

Incentivized GUSD adoption

- MakerDAO fee spikes driven by Gemini payments. Gemini is utilizing MakerDAO to boost the adoption of its stablecoin, Gemini Dollar (GUSD). They currently offer an attractive 1.25% annual yield on GUSD deposits in the PSM-GUSD-A vault.

- Gemini has incentivized a significant part of GUSD to be held in Maker vaults. Over 80% of the total Gemini USD supply is currently held in the PSM-GUSD-A vault.

- This incentive program is contributing significantly to MakerDAO's revenue. Gemini's payments have emerged as the primary source of fees for the protocol. In the past 180d, MakerDAO received $2.6 million in revenue from incentive payments.

LUSD's rising demand

- USDC depeg and Paxos lawsuit underscore the importance of on-chain collateral. The recent USDC depeg, coupled with BUSD issuer Paxos’ lawsuit with the SEC, has led to a growing interest in stablecoins that offer fully on-chain collateral. This is shown by the consistent rise in LUSD demand since March 11th. In Q1, the overall LUSD supply increased by over 50%. It was one of the few stablecoins to grow during this time.

- Bank failures and regulatory risks plague centralized stablecoins. The challenges faced by centralized stablecoin issuers, such as Paxos and Circle, stem from various counterparty risks and regulatory scrutiny. These problems have emphasized the value of censorship-resistant alternatives like LUSD.

- Binance listing boosts Liquity’s growth and adoption. Liquity’s growth has also been propelled by its listing on Binance. Seen as the exchange’s new favorite substituent for Paxos, this development has caused the price of LQTY to rise sharply, further boosting Liquity’s adoption.

Abracadabra's decline

- Abracadabra.money’s momentum continues to diminish. Abracadabra.money, a once prominent stablecoin protocol, has seen a continuous decline in the usage of its MIM stablecoin, and the price of its SPELL governance token. A similar pattern is common among many community-driven DeFi protocols with high token inflation, such as LooksRare and SushiSwap.

- Unfortunate yet preventable events have troubled the protocol. Numerous setbacks have contributed to Abracadabra.money's challenges over the past 18 months. These include key team member controversies, and 30% of the protocol’s collateral being in FTT during the FTX meltdown. With no clear direction as of now, it remains to be seen if the current team can make a change for the better.

- Look for fundamental value and be wary of excess token inflation. Investors should assess factors such as team composition, operational processes, and management structure when evaluating projects. It is also crucial to consider the genuine value capture potential of a token and evaluate it against token emissions.

EURe supply growth

- EURe’s outstanding supply increased by 66% during the past 30d. EURe's outstanding supply on Gnosis has shown steady growth since its launch in January, while the outstanding supply on Ethereum and Polygon saw a large spike earlier this month.

- Individual addresses significantly contributed to growth. On Gnosis, the largest net contributor accounted for 75% of the 746k increase, whereas on Polygon, the largest net contributor was responsible for 64% of the 906k surge. Interestingly, on Ethereum, the largest net contributor added 2 million to the supply, while the total supply only increased by 1.78 million, implying that the remaining active users decreased the supply by 220k over the past 30d period.

- It is vital to analyze underlying drivers when examining smaller protocols. While the absolute growth in outstanding supply was predominantly driven by a few individual addresses, the other 828 active users over the past 30d still contributed to strong relative growth on Gnosis and Polygon.

USDC’s layer 2 growth

- Layer 2 blockchains witness a surge in USDC transfer volume. A remarkable growth in monthly transfer volume for USDC on Arbitrum and Optimism has been observed since mid-2022, with an almost ten-fold increase from approximately $6 billion to nearly $60 billion in March 2023.

- Low fees and incentives drive user adoption. The expansion in layer 2 blockchain usage can largely be attributed to reduced fees and, to some extent, incentivized activity. Optimism features several dApps offering OP incentives to users. In a similar vein, Arbitrum recently distributed $120 million worth of ARB tokens to DAOs within its ecosystem, enabling these DAOs to retroactively reward users or stimulate liquidity and usage through new ARB incentives.

- As layer 2 blockchains gain traction, a notable shift towards retail adoption and smaller transactions emerges, highlighting the potential for a more inclusive and accessible DeFi landscape. The growing adoption of layer 2 scaling solutions is particularly indicative of increased retail usage and smaller-scale transfers, as evidenced by underlying on-chain data. Median transfer sizes on Arbitrum and Optimism amounted to $107 and $32, respectively, while Ethereum's $1,250 median is considerably higher. Observing whether layer 2 solutions can maintain and continue expanding their organic user bases will be crucial in the coming months.

Video of the week

Wouter Kampmann, Co-Founder of MakerDAO Sustainable Ecosystem Scaling (SES) – a Core Unit that focuses on sustainably growing the Maker Protocol’s moats by removing barriers between decentralized workforce, capital, and work – joined us for an episode to discuss the basics of MakerDAO and the SES Core Unit.

Timestamps:

00:00 Introduction

00:55 MakerDAO and the DAI stablecoin

03:03 What are Core Units?

03:33 The Sustainable Ecosystem Scaling Core Unit

04:40 The expenses dashboard & its purpose

07:05 How is MakerDAO structured as an on-chain organization?

09:42 Overview of the different Core Units & what they do

12:45 How are the budgets for Core Units determined?

15:30 How have budgets and headcount developed over time?

17:06 Overview of Core Unit expense reports

19:42 Forecast & MKR Vesting -tabs

21:20 Auditor cycle – quality control and auditing of expense reports

24:40 What’s next for MakerDAO?

Tweet of the week

Follow us on Twitter for daily updates

Data-driven due diligence in crypto:

— Token Terminal 📊 (@tokenterminal) April 24, 2023

1⃣Onchain data

✅Easy to access

2⃣Open source code

✅ Easy to verify

3⃣New deployments, deprecated contracts, etc.

❌Difficult to assure completeness (until now) pic.twitter.com/eYXW74aAmU

Product tip of the week

Tips for getting the most out of Token Terminal

We've now added 'Show as aggregated' option to our market sector dashboards. This way, you can easily view the total fees, volumes, or DAUs for a specific market sector.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

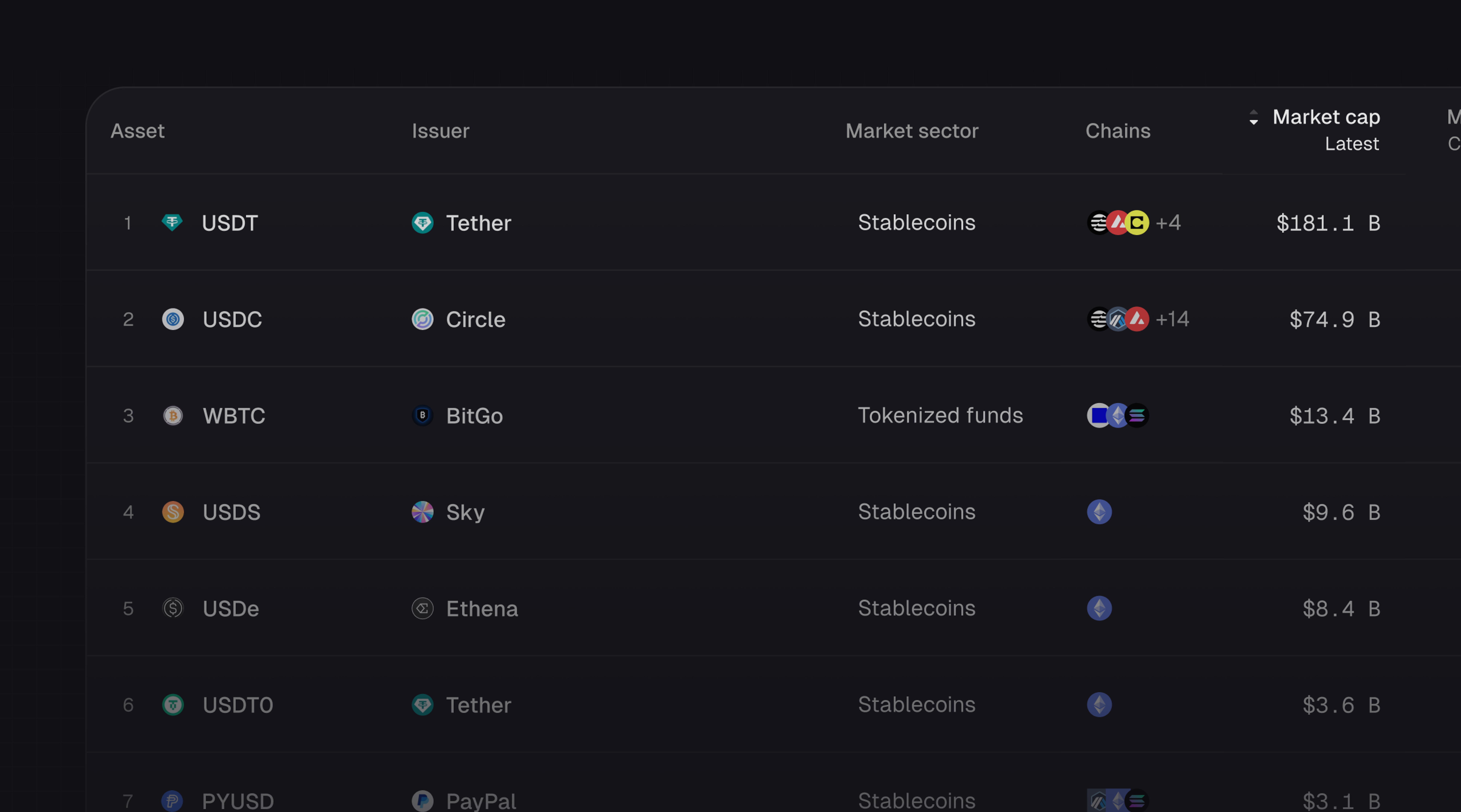

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.