Research

Saving money is hard

Token Terminal

•

PoolTogether

Get rich or Dai tryin’.

Saving money is hard

According to a Federal Reserve Board survey from 2015 on the economic well-being of US households, 46% of participants responded that they would have difficulties in covering expenses of $400 or more in an emergency situation. The middle class currently lives from paycheck to paycheck and has a hard time stashing money for rainy days. Currently, 67 million Americans can be considered unbanked or underbanked, a large group of people that have long been ignored by financial innovation.

Richard Thaler, a pioneer within the field of behavioural economics, said in a 2015 Wall Street Journal interview that saving for retirement is an archetypal behavioural economics problem. According to Thaler, long-term saving is cognitively hard — as you need to figure out how much to save in addition to performing self-control over your spending habits. One solution that has been brought to market is the 401(k). The 401(k) is a defined-contribution retirement plan, which means that a person sets money aside automatically in the plan (employers provide and sometimes proportionally match the contributions). Employees may choose to opt out of the 401(k), but they’re opted in by default — proving the passive model to be beneficial for getting people to save their money. Thaler remarked that these default plans are “probably behavioural economists’ greatest success story”.

These default plans are not however available to everyone. Factory gigs conveyed through job centres and heaps of other low-end jobs do not offer retirement plans to millions of Americans. Even if a similar plan was available, it does nothing to encourage short-term savings to combat unexpected situations.

Combining savings accounts and lotteries

Craving for a way out

According to a 2019 study, the 2017 total spending on lottery tickets in the US was 70 billion dollars — or an average of 220 dollars per citizen. Lower-income citizens spend a proportionally larger percentage of their income on lottery than those with a higher-income. A 1999 study by Duke University found that nearly half of all households with incomes below 25,000 dollars regularly played the lottery.

When searching for answers on why people choose to play the lottery despite the low chances of winning, one might easily dismiss it as ignorance. However, according to a 2008 article in the Journal of Behavioral Decision Making, researchers made the argument that lotteries are enticing for lower-income people as they offer a chance at an otherwise unattainable substantial economic gain. The lottery may seem like the only way out for several people, hence they keep playing it.

Enter prize-linked savings programs

In 2001, Timothy Flacke and Peter Tufano founded Commonwealth, a financial program to benefit vulnerable lower-income people. The intent was to create a savings program, which would award prizes randomly for the people participating in the savings program. Tufano got the idea from Premium Bonds, which were introduced in the UK in the 1950s. Buyers of these bonds entered a lottery-like system with regular prizes of up to 1 million pounds, which were paid out of the pooled interest generated by the bonds.

Following a number of legal hurdles, it turned out that the laws of Michigan would allow for Commonwealth to give their program a try. Together with their partners they created a program called Save to Win, which offered cash prizes on a monthly basis through the Michigan Credit Union League. The program included a single large prize, which was awarded less frequently, and a series of smaller prizes, which were awarded more frequently. The smaller frequent payouts resulted in hyperbolic discounting, i.e. participants valued short-term possibilities over long-term gains. The possibility to win 50 dollars immediately instead of earning 200 dollars through a small interest over several years was a lot more intriguing for the participants. Having the even slimmer possibility for a grand prize was the icing on the cake.

Fast forward to the present-day, retail giants such as Walmart have also built their own programs around this approach. Walmart’s service allows customers to put up to $500 into an account. Once the money is in the account, each dollar participates in one of 1,000 different cash prizes monthly.

However, these services are local and cannot serve global audiences. With 2 billion unbanked people in the world, a global prize-linked savings program could offer an improvement to people’s saving habits worldwide.

PoolTogether as a global PLS program

PoolTogether is an Ethereum-based no-loss lottery game, where users provide liquidity to a lending pool on Compound. Users contribute to the pool by purchasing lottery tickets, which are 1:1 to Dai and USDC. The lending pool earns interest on the principal, and after a certain period of time, the interest is randomly allocated to a user who contributed to the lending pool. PoolTogether is non-custodial, which means that users can withdraw their principal at any time. Therefore, the alternative cost of joining PoolTogether is the interest on personally lent Dai or USDC.

PoolTogether user and funds flow.

Currently, the pooled interest from Dai is rewarded to one winner per week. Going forward, PoolTogether could emulate proven concepts from previous PLS programs and add smaller prizes to be paid out more frequently. PoolTogether already provides biweekly payouts of USDC interest, but there is still heaps to experiment in this regard.

In order to increase the amount of interest paid out to the winner/winners, PoolTogether lending pools also include “sponsored Dai”. Sponsored Dai is an amount of Dai participating in the lending pool to generate more interest, but does not participate in the lottery. This model presents an effective way for venture capitalists to improve the value proposition of companies such as PoolTogether, as part of their capital can be used to grow the pool through sponsored Dai.

As PoolTogether’s infrastructure, namely Ethereum and Compound, exists fully on the Internet, its services are transparent and globally accessible. PLS programs are proven to improve the savings behaviour of lower-income people, who otherwise are not allured by the promise of a small interest on their principal.

PoolTogether has the opportunity to improve people’s savings habits at a global scale.

Token Terminal provides financial and business metrics on crypto protocols — metrics we’re used to seeing applied to traditional companies, e.g the P/E ratio. Crypto protocols operate like traditional businesses, only they do it directly on the Internet.

For more, check out Token Terminal’s website and Twitter.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

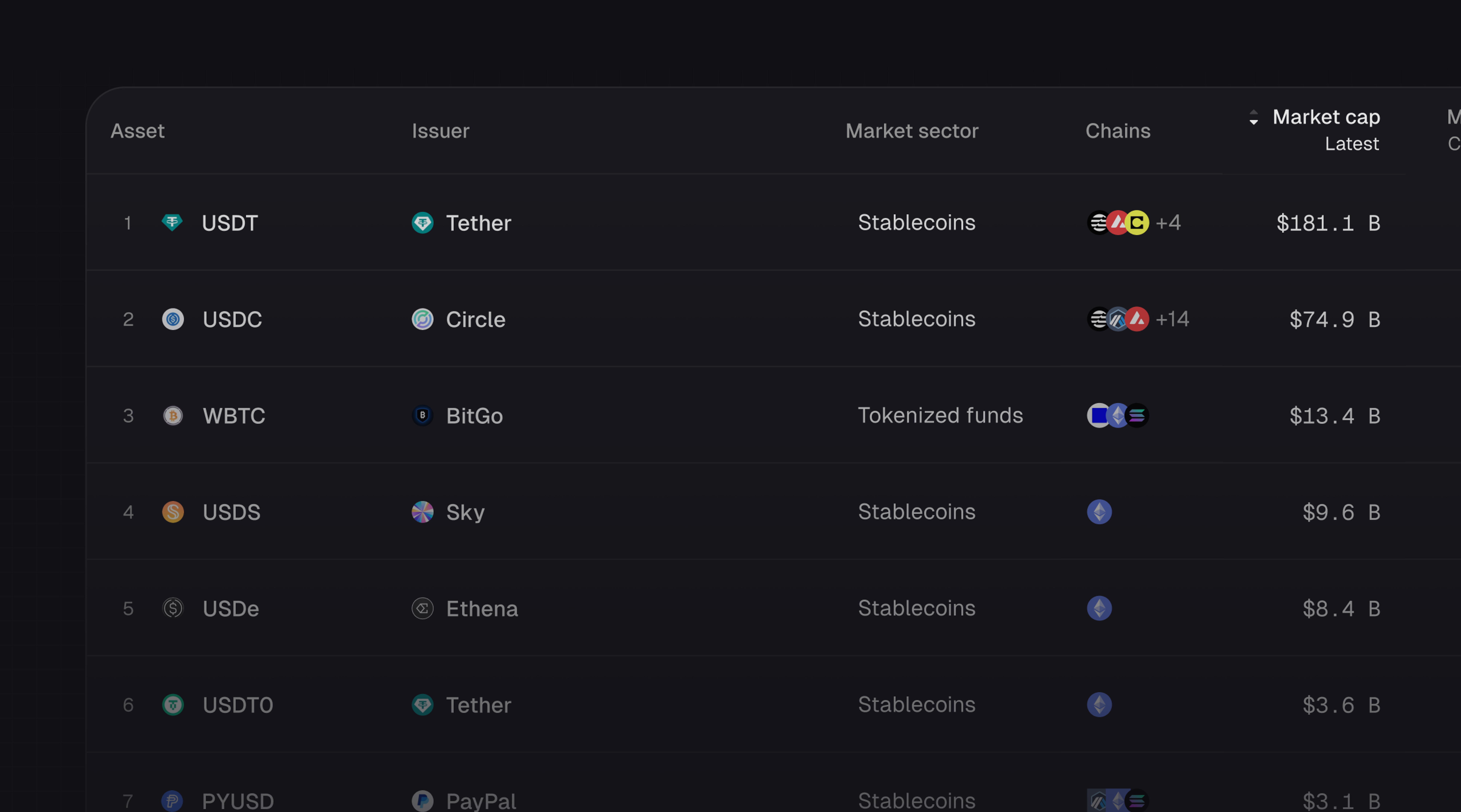

Introducing Tokenized Assets

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.